: Complete Guide](https://file-host.link/website/cloudtech-ff604p/assets/refined-images/1783584990200000_74c68dd7d9904f9aa6eb455f259b1f36/360.webp)

Introduction

Every fintech lender running performance marketing faces the same painful gap: a prospect submits a loan inquiry, and somewhere between that form submission and the first human callback, the lead goes cold. That window is where conversion is lost. AI voice bots exist specifically to close it.

This guide is for fintech lenders, digital lending platforms, mortgage companies, and financial services sales teams running paid lead campaigns. High-intent loan leads are time-sensitive.

Research from Velocify's analysis of millions of internet-generated leads shows that calling within one minute produces a 391% conversion improvement over waiting 30 minutes — and mortgages were among the primary product categories studied.

What follows is a complete operational guide covering:

- What an AI voice bot for loan lead qualification actually is

- How the end-to-end process works

- Which qualification criteria it evaluates

- US compliance requirements you must address before going live

- Where the technology falls short and when not to use it

Key Takeaways

- AI voice bots can contact new loan inquiries in under 60 seconds, versus a typical 15–45-minute manual callback window

- They conduct structured, adaptive qualification conversations — income, employment type, loan obligations, desired amount, and timeline — without a human agent

- Post-call data maps automatically to CRM or loan origination systems, delivering a warm, pre-qualified handoff to loan officers

- Every US deployment must address TCPA consent, DNC registry scrubbing, and GLBA data handling

- AI handles qualification at scale; complex structuring and relationship-sensitive decisions still require licensed loan officers

What Is an AI Voice Bot for Fintech Loan Lead Qualification?

An AI voice bot for fintech loan lead qualification is an automated outbound calling system that uses natural language processing to contact new loan inquiries, conduct structured qualification conversations, and route scored leads to human loan officers. No manual agent involvement is required at the initial stage.

The Core Problem It Solves

Speed is everything in loan origination. The MIT/InsideSales.com Lead Response Management Study, which analyzed 15,000+ leads and 100,000 call attempts over three years, found that the odds of contacting a lead drop 100x if you call at 30 minutes versus 5 minutes — and the odds of qualifying that lead drop 21x. Most lending teams aren't calling within 5 minutes — not even close.

An AI voice bot closes that gap by placing the outbound call within seconds of form submission — while the prospect's intent is still peak.

How It Differs from IVR

Traditional IVR routes calls through rigid keypad menus and keyword matching. It has no conversational memory and cannot adapt to how a borrower naturally responds.

An AI voice bot uses large language models to hold a multi-turn, adaptive conversation. It understands intent regardless of phrasing, retains context across the entire interaction, and adjusts follow-up questions based on what the prospect actually says.

Here's how those capabilities compare at a glance:

| Capability | IVR | AI Voice Bot |

|---|---|---|

| Conversational memory | None | Full multi-turn context |

| Response flexibility | Fixed keypad menus | Adapts to natural speech |

| Follow-up questions | Pre-scripted only | Dynamic, based on responses |

| Intent understanding | Keyword matching | Large language model (LLM) |

How It Differs from a Chatbot

The chatbot comparison is equally important. Chatbots operate on text channels and are typically inbound. AI voice bots make outbound calls, on the phone channel, at the moment of highest intent — which matters in loan origination where most leads arrive via digital forms and expect a callback, not a chat window.

How the AI Voice Bot Loan Qualification Process Works

The end-to-end flow:

Lead submits inquiry form → webhook fires → CRM record created → outbound call placed automatically → NLP qualification conversation runs → data extracted and scored → lead tagged and routed → loan officer receives pre-qualified briefing

Step 1: Trigger and Outreach

When a prospect submits a loan inquiry form, the submission triggers a webhook that activates the voice bot within seconds. The telephony layer (commonly built on Amazon Connect, AWS's cloud contact center) places the outbound call immediately.

The underlying AWS stack that fintech companies typically use for this infrastructure:

- Amazon Connect — handles outbound telephony and call orchestration

- Amazon Lex — provides the NLP engine for conversational dialogue (note: new deployments should use Lex V2, as Lex V1 support ends September 2025)

- Amazon Polly — synthesizes natural-sounding voice responses from text

- AWS Lambda — processes the incoming lead event and triggers the outbound call in milliseconds

- Amazon API Gateway — serves as the secure entry point for the form submission event

If the call goes unanswered, a parallel SMS or email follow-up is dispatched and a retry sequence is scheduled automatically. Fintech teams working with an AWS Advanced Tier Partner like Cloudtech can architect and deploy this full stack on a compliant, scalable cloud foundation.

Step 2: The Qualification Conversation

The bot opens every call with a disclosure identifying itself as an automated system, which federal regulations require before any automated outreach continues. It then runs a sequence of loan-specific qualifying questions.

The conversation is adaptive: the bot listens to each response and adjusts follow-up questions in real time, rather than following a rigid script. Branching logic responds to what the prospect actually says — for example:

- A self-employed applicant gets follow-ups on income documentation and business tenure

- A salaried applicant is routed toward employer verification and pay stub confirmation

- A prospect expressing urgency sees compressed pacing and faster handoff routing

Step 3: Lead Scoring and Routing

Once the conversation concludes, the system scores the lead against predefined criteria and assigns a disposition:

| Disposition | Meaning |

|---|---|

| Qualified | Meets income, employment, and timeline criteria |

| Follow-Up Required | Partial information; needs additional outreach |

| Not Interested | Prospect declined or disqualified |

| Callback Requested | Prospect asked for a human to call at a specific time |

The lead is tagged for the appropriate loan officer based on product type, loan amount tier, or geography. A full conversation summary posts automatically to the CRM or LOS — so the loan officer enters the follow-up call already knowing the prospect's situation, not asking the same questions over again.

Key Loan Qualification Criteria an AI Voice Bot Evaluates

The standard qualification framework for loan leads extends the BANT model (Budget, Authority, Need, Timeline) — originally developed for enterprise sales — into lending-specific territory.

Applied to loan qualification:

- Budget — Can this prospect actually service the debt? Income level and existing obligations

- Authority — Is this the primary applicant, or a co-borrower situation?

- Need — What is the loan purpose, and how urgent is it?

- Timeline — Immediate funding need or planning ahead?

BANT gets the conversation started. A well-configured loan qualification bot goes further, capturing the data points underwriters actually need:

- Monthly gross income

- Employment type (salaried, self-employed, contractor)

- Years at current employer

- Existing monthly debt obligations

- Desired loan amount and preferred term

- Approximate credit score range (self-reported)

- Timeline to fund

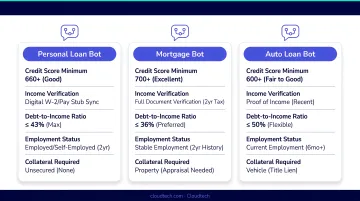

Why Script Customization by Loan Product Matters

A personal loan bot asks fundamentally different questions than a mortgage bot. A home equity bot needs to capture property value and existing lien information. An auto loan bot focuses on vehicle purchase timeline and down payment availability.

Using a generic script across all loan types reduces qualification accuracy and frustrates prospects who get asked irrelevant questions. Each loan product requires its own conversation flow configured to match the underwriting criteria and borrower profile for that product.

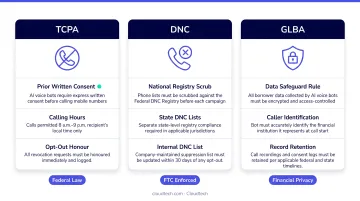

Compliance and Regulatory Requirements for Loan Lead Qualification Calls

Most teams underestimate this part. Deploying an AI voice bot for loan-related outbound calling without addressing these requirements creates significant legal exposure.

TCPA Requirements

The Telephone Consumer Protection Act requires prior express written consent before placing automated calls to cell phones. Key points:

- Consent must be captured at the point of lead form submission using compliant consent language

- The FCC's one-to-one consent rule was vacated by the Eleventh Circuit in January 2025 and subsequently repealed — the prior express written consent standard remains the operative requirement

- Consumers may revoke consent at any time in any reasonable manner; revocation must be honored within 10 business days

DNC Registry Scrubbing

Per FTC requirements for telemarketers and sellers:

- Calling lists must be synchronized with the National Do Not Call Registry at least every 31 days

- Sellers must maintain their own Subscription Account Number (SAN)

- Civil penalties can reach $53,088 per call

Call Recording Consent

All-party consent states include California, Florida, Maryland, Massachusetts, New Hampshire, Pennsylvania, and Washington — meaning all parties on the call must consent to recording. Most other states follow one-party consent, but this varies by jurisdiction and context. Verify state-by-state before deployment.

GLBA Data Handling

The FTC's Safeguards Rule under GLBA requires covered financial institutions to:

- Maintain a written information security program

- Encrypt customer information at rest and in transit

- Implement multi-factor authentication

- Maintain authorized-user access logs

- Securely dispose of customer information no later than two years after last use (unless retention is legally required)

AWS infrastructure with proper security configurations supports GLBA-aligned data handling. That said, the financial institution remains responsible for implementing and validating the controls — your legal and compliance teams need to sign off on the overall program, not just the technical setup. Cloudtech's financial services cloud engagements include security configuration aligned with GLBA requirements, but your institution's counsel must validate the final compliance posture.

Before going live: Have your voice bot deployment reviewed by legal counsel familiar with TCPA, CFPB guidance, and applicable state consumer finance laws. Requirements differ by state, by loan product type, and sometimes by the channel through which consent was collected — so a one-size-fits-all review rarely covers everything.

Common Misconceptions and Limitations

Misconception 1: AI Voice Bots Replace Loan Officers

They don't. AI voice bots handle the initial qualification layer only. Complex loan structuring, rate negotiation, exception underwriting, and any interaction requiring licensed advice must involve a human loan officer.

Teams that deploy voice bots expecting them to close loans will be disappointed. Teams that deploy them to fill the pipeline with pre-qualified leads will see results.

Misconception 2: Any Voice Bot Will Work

Loan lead qualification requires:

- Financial-services-specific conversation flows, not generic scripts

- TCPA and GLBA compliance controls baked into the architecture

- Native integration with LOS platforms like Encompass (used by more than 40% of the mortgage industry) or lead management systems like Velocify, plus the team's CRM

A generic IVR or off-the-shelf chatbot cannot meet these requirements without substantial customization. The compliance and integration requirements alone make financial services a distinctly more complex deployment than most other industries.

That said, even a well-configured voice bot isn't the right tool in every situation.

Where AI Voice Bots Are Not the Right Fit

- Jumbo mortgages and complex commercial loans: Borrowers at this level expect their first conversation to be with a senior loan officer, not an automated system

- Very low lead volume: If your team can manually respond within five minutes, the ROI case for automation weakens considerably

- Non-compliant lead sources: Without explicit TCPA-compliant consent language captured on the lead form, you cannot legally place automated outbound calls to those prospects

Frequently Asked Questions

How is an AI voice bot different from an IVR for loan lead qualification?

Traditional IVR uses rigid menus and keyword matching with no conversational memory. An AI voice bot uses NLP to hold an adaptive, multi-turn conversation — understanding intent regardless of phrasing and retaining context throughout — which results in a more natural borrower experience and significantly higher qualification completion rates.

What compliance requirements apply to AI voice bots making loan-related calls in the US?

The core requirements are TCPA written consent for automated calls to cell phones, DNC registry scrubbing before each dial, AI disclosure at call start, state-specific call recording consent (all-party vs. one-party varies by state), and GLBA-compliant data storage. Validate all of these with legal counsel before deployment.

What loan qualification questions does an AI voice bot typically ask?

The core data points: monthly gross income, employment type, existing debt obligations, desired loan amount and term, credit score awareness, and funding timeline. The script should be customized per loan product type — a mortgage bot and a personal loan bot ask meaningfully different follow-up questions.

How does an AI voice bot integrate with loan origination systems and CRMs?

Integration happens via webhooks and APIs that map structured conversation data to the correct fields in the LOS or CRM — such as Encompass, Salesforce, or HubSpot. This triggers deal stage updates, routing assignments, and follow-up tasks automatically after each call, giving loan officers a clean handoff without manual data entry.

How quickly can an AI voice bot contact a new loan inquiry?

A properly configured system places the outbound call within 60 seconds of form submission. MIT/InsideSales.com research shows lead qualification odds drop 21x when response time stretches from 5 to 30 minutes — a window most lending teams can't hit manually.

What results can fintech lenders realistically expect from deploying an AI voice bot?

Treat vendor claims cautiously — published benchmarks for loan-specific voice bot ROI are limited. Velocify's multi-million-lead analysis does show a 391% conversion lift from calling within one minute. Actual results hinge on script quality, CRM integration depth, lead source compliance, and the human handoff process.