Introduction

McKinsey estimates generative AI could deliver $200–$340 billion in annual value potential to the banking sector — equivalent to 2.8%–4.7% of total industry revenues — if fully implemented across banking operations. That number has moved GenAI from an exploratory technology to a board-level priority almost overnight.

The pressure is real on multiple fronts. Banks today are contending with:

- Manual back-office workflows that drain staff productivity

- Fraud losses that exceeded $485 billion globally in 2023

- Compliance burdens consuming 11–15% of payroll at smaller community banks

- Customers who now expect Amazon-style personalization from their financial institutions

Generative AI addresses all four pressure points, which explains why adoption is accelerating across institutions of every size.

This guide covers everything you need to know: what generative AI actually means in a banking context, the highest-impact use cases, real-world results from leading institutions, key benefits, implementation challenges, and how to get started without overreaching.

Key Takeaways

- GenAI generates new content, insights, and decisions — not just classifications like traditional rule-based AI

- The highest-ROI use cases span customer service, fraud detection, credit processing, and regulatory compliance

- Mastercard, OCBC, Klarna, and SouthState Bank are already seeing measurable results from live GenAI deployments

- Data privacy, legacy system integration, and model explainability are the core challenges banks must resolve before scaling

- AWS tools — Amazon Bedrock, SageMaker, and Textract — offer a practical, secure foundation for regulated GenAI workloads

What Is Generative AI in Banking?

Beyond Classification and Prediction

Traditional AI in banking does one thing well: it classifies or predicts from structured data using pre-defined rules. Flag a transaction over $10,000. Approve a loan if the FICO score exceeds 720. Deny a claim if a field is missing.

Generative AI works differently. NIST defines it as "the class of AI models that emulate the structure and characteristics of input data in order to generate derived synthetic content," including text, analysis, code, and decisions. In practice, GenAI doesn't just check boxes.

It reads a loan application and drafts a credit memo. It scans 10,000 transactions and writes a suspicious activity report. It answers a customer's mortgage question in plain English, in real time, in their preferred language.

For banking, that distinction matters enormously.

How It Applies in Financial Services

Banks sit on vast volumes of unstructured data — regulatory filings, customer communications, loan documents, transaction narratives — that traditional AI can't process meaningfully. GenAI, powered by large language models (LLMs) and deep learning, can ingest this data and:

- Automate decisions that previously required human review

- Generate compliance reports, credit memos, and customer responses at scale

- Identify patterns across millions of data points in milliseconds

- Deliver personalized interactions without proportional headcount increases

Where Adoption Stands Today

Adoption is moving from pilot to production. KPMG found that 60% of banks plan to use GenAI to bridge talent gaps and automate up to 20% of daily tasks. Among financial services GenAI pioneers tracked by Deloitte, 76% allocate 20% or more of their AI budgets specifically to GenAI — and 43% have already given GenAI access to more than 40% of their workforce.

Banks still in the pilot phase risk ceding ground on cost efficiency, compliance speed, and customer experience to competitors who have already moved to production.

Key Use Cases of Generative AI in Banking

Customer Service and Virtual Assistants

LLM-powered virtual assistants now handle account inquiries, transaction history reviews, financial product recommendations, and dispute resolution — 24/7, across multiple languages, in natural conversational language. Unlike earlier chatbots that required rigid scripted flows, GenAI assistants understand intent, pull relevant account context in real time, and escalate complex cases to human agents with a full conversation summary already prepared.

Klarna's AI assistant processed 2.3 million conversations in its first month — two-thirds of all customer service chats — while cutting average resolution time from 11 minutes to under 2 minutes. That's the equivalent work of 700 full-time agents, across 35+ languages.

For mid-sized banks, the same architecture applies at smaller scale: a well-implemented GenAI assistant reduces call center volume, improves first-contact resolution rates, and frees staff for higher-value advisory work.

Fraud Detection and Prevention

Rule-based fraud systems work until fraudsters learn the rules. GenAI doesn't wait to be programmed — it continuously analyzes behavioral patterns, generates synthetic fraud scenarios to train detection models, and identifies emerging attack vectors that no predefined rule would catch.

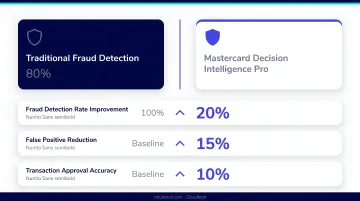

Mastercard's Decision Intelligence Pro scans 1 trillion data points to assess transaction legitimacy in under 50 milliseconds, boosting fraud detection by 20% on average — and as high as 300% in specific fraud categories — while cutting false positives by more than 85%.

That false-positive reduction matters as much as the detection improvement. Legitimate transactions incorrectly flagged create customer friction, generate complaint volume, and erode trust. GenAI addresses both sides of the problem simultaneously.

Credit Scoring, Loan Processing, and Underwriting

Traditional credit models evaluate a narrow set of structured signals. GenAI analyzes a broader picture — spending behavior, transaction history, external financial indicators — to generate more nuanced risk assessments faster, and with less reliance on a single score.

The speed gains in credit workflows are measurable. McKinsey tracked a commercial client-monitoring use case where GenAI tools reduced time to answer climate-risk underwriting questions from over two hours to under 15 minutes — a roughly 90% reduction — with 90% correctness in synthesized responses.

GenAI also automates the document-heavy side of lending:

- Generates credit memos, loan summaries, and required documentation automatically

- Reduces loan officer time on paperwork, freeing capacity for borrower relationships

- Enables higher loan volumes without adding underwriting headcount

Regulatory Compliance and Document Processing

Compliance is one of the clearest near-term wins for GenAI in banking. Document-heavy workflows — KYC filings, AML reports, regulatory submissions, contract reviews — are labor intensive, error-prone, and expensive at smaller institutions. Community banks spend 11–15.5% of payroll on compliance versus 6–10% at larger banks, according to CSBS data.

GenAI addresses this through:

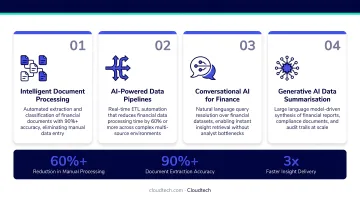

- Intelligent document processing: OCR and NLP extract, classify, and validate data from unstructured documents automatically

- AML pattern detection: Models simulate laundering scenarios, identify complex cross-account patterns, and surface real-time alerts before suspicious activity escalates

- KYC automation: LLMs scan customer data and external sources to assess compliance risk without rigid templates

Airwallex deployed a GenAI KYC tool that reduced false-positive alerts by 50% and increased fully automated onboarding by 20% across more than 100,000 businesses — without sacrificing compliance accuracy.

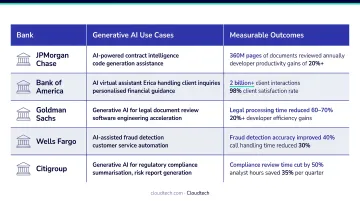

Real-World Examples of Banks Using Generative AI

| Institution | Use Case | Reported Outcome |

|---|---|---|

| Mastercard | Decision Intelligence Pro fraud detection | 20% avg. fraud detection improvement; 85%+ false positive reduction |

| OCBC Bank | OCBC GPT — internal GenAI assistant for 30,000 employees | Writing and research tasks completed ~50% faster |

| Klarna | AI customer service assistant across 35+ languages | 2.3M chats handled; resolution time cut from 11 min to <2 min |

| Airwallex | GenAI KYC copilot | 50% fewer false-positive alerts; 20% more fully automated onboardings |

| SouthState Bank | Internal ChatGPT agent ("Tate") for employee productivity | Search time dropped from ~7 min to <32 sec; estimated $442K annual savings per 100 users |

SouthState Bank is worth noting for smaller and mid-sized institutions. It's a community bank that deployed Azure OpenAI around a single, focused use case — employee productivity — and hit measurable ROI within weeks. The infrastructure investment was modest; the productivity gains were not. That combination is what makes this model worth studying for institutions that aren't operating at Mastercard's scale.

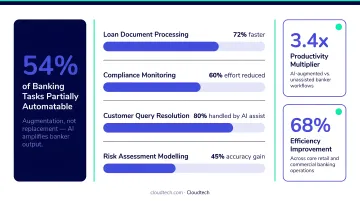

Key Benefits of Generative AI for Financial Institutions

Generative AI delivers measurable gains across the core priorities of any financial institution — customer growth, operating costs, risk, and compliance. Here's what the data shows:

Personalized Customer Experience at Scale

GenAI enables proactive financial advice, tailored product recommendations, and responsive support without proportional headcount growth. McKinsey research on AI-powered next-best-experience capabilities shows customer satisfaction improvements of 15–20% and revenue improvements of 5–8% in financial services contexts.

Operational Efficiency and Cost Reduction

Accenture estimates that 73% of time spent by U.S. bank employees has high potential to be impacted by GenAI:

- 39% through full automation of routine tasks

- 34% through augmentation of existing workflows

- 22–30% productivity improvement projected for early adopters over three years

PwC projects that fully embracing AI could drive a 15-percentage-point improvement in bank efficiency ratios.

Faster, More Accurate Risk Management

GenAI evaluates market trends, customer portfolios, and operational data simultaneously — producing risk assessments that catch credit risk, fraud signals, and market volatility faster than traditional models with less manual intervention at each step.

Stronger Regulatory Compliance Posture

Automated extraction, organization, and summarization of regulatory data cuts the time and error rate in compliance reporting. Banks can also monitor regulatory changes continuously rather than relying on periodic manual reviews.

Common Challenges in Implementing Generative AI in Banking

Data Privacy and Regulatory Compliance

GenAI models require access to sensitive financial data. Sharing that data with third-party cloud providers creates exposure under GDPR, CCPA, and sector-specific regulations — and the CFPB has made clear there is "no special exemption for artificial intelligence" when it comes to adverse action notification requirements or credit decision fairness.

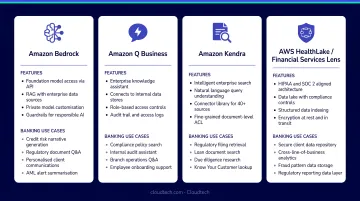

The practical solution is to deploy GenAI within your own secure cloud environment rather than routing data to external APIs. Services like Amazon Bedrock allow banks to access foundation models without customer data being used for model training or shared with third-party providers.

AWS publishes compliance documentation for Bedrock covering ISO, SOC, CSA STAR Level 2, and HIPAA eligibility. For banks mapping their regulatory posture, that documentation is a useful starting point.

Legacy System Integration

Most core banking systems weren't designed to interface with modern AI frameworks. Full-stack overhauls aren't necessary. API-led architectures and cloud migration strategies allow banks to bridge legacy systems with modern AI layers incrementally, connecting existing data sources to GenAI workflows without replacing the core infrastructure that keeps the bank running.

An AWS-certified implementation partner like Cloudtech handles this integration layer — connecting legacy systems to AWS-native AI services with security and compliance guardrails built in from the start.

Model Explainability and Bias

Regulators demand clear explanations for AI-driven decisions in credit scoring, loan approvals, and fraud flagging. The CFPB's 2023 guidance explicitly states that lenders must provide accurate and specific reasons for credit denials — regardless of how complex the underlying model is.

Mitigations include:

- Interpretability tools (SHAP values) to surface the factors driving individual decisions

- Human-in-the-loop review at key decision points before adverse actions are taken

- Model monitoring frameworks to detect performance drift and emerging bias over time

How to Get Started with Generative AI in Banking

Start With High-Value, Lower-Risk Use Cases

Don't attempt enterprise-wide GenAI deployment as the first step. SMBs and mid-sized banks should begin with targeted, contained applications:

- Internal document summarization (policy documents, regulatory updates)

- Fraud alert triage (GenAI reviews flagged transactions and drafts analyst summaries)

- Customer FAQ chatbots for account inquiries and product questions

- KYC document classification and pre-screening

These generate quick ROI, build organizational AI literacy, and reveal integration challenges at manageable scale before expanding.

Build on a Secure, Scalable Cloud Foundation

AWS provides purpose-built infrastructure for deploying GenAI in regulated industries:

- Amazon Bedrock: Managed access to foundation models with data protection controls and compliance certifications

- Amazon SageMaker: Custom model training, evaluation, and MLOps workflows

- Amazon Textract: Intelligent document processing for financial documents, including loan applications, KYC filings, and compliance records

- Amazon Q Business: Natural language interfaces for querying financial data without requiring technical expertise

Cloudtech's Cloud Foundation package establishes this environment by deploying secure multi-account AWS infrastructure with Control Tower, IAM governance, KMS encryption, and compliance automation, built to support GenAI workloads immediately. For banks without deep in-house AWS expertise, working with an AWS Advanced Tier partner cuts implementation timelines from months to weeks while keeping security and cost under control.

Establish Governance Before Scaling

A solid infrastructure foundation is only half the equation. Successful GenAI programs in banking require governance from the start, not retrofitted after problems emerge:

- Data governance frameworks that define what data GenAI can access and how it's protected

- Model monitoring to detect drift, bias, and unexpected outputs

- Human oversight at decision points with material financial or regulatory consequences

- Explainability documentation that satisfies audit requirements and regulator inquiries

Banks that establish these practices early move faster in the long run. Those that can demonstrate transparent, well-governed AI to regulators and customers face fewer compliance delays when scaling than those that treat governance as an afterthought.

Frequently Asked Questions

How can generative AI be used in banking?

GenAI spans front, middle, and back-office functions: customer service chatbots and virtual assistants, real-time fraud detection, credit risk assessment and loan document generation, KYC and AML compliance automation, and regulatory reporting. Banks are deploying it wherever there's high-volume, document-heavy, or decision-intensive work.

What is the difference between generative AI and traditional AI in banking?

Traditional AI classifies or predicts from structured data using pre-defined rules — it answers "yes" or "no" based on thresholds. Generative AI creates new content, synthesizes insights from unstructured data, and adapts to novel scenarios. In banking, that means generating credit memos, drafting compliance reports, or explaining a fraud flag in plain language — work that rule-based systems simply cannot perform.

How does generative AI improve fraud detection in banks?

GenAI monitors transactions in real time, generates synthetic fraud scenarios to train detection models, and identifies emerging behavioral patterns that rule-based systems miss. It also reduces false positives — Mastercard's Decision Intelligence Pro cut false positives by over 85% — preventing legitimate customer transactions from being incorrectly flagged.

What are the biggest challenges of implementing generative AI in banking?

Three challenges consistently emerge during implementation:

- Data privacy: keeping models compliant when accessing sensitive financial data

- Legacy integration: connecting GenAI to core banking systems not built for modern AI frameworks

- Explainability: ensuring AI-driven credit and fraud decisions satisfy regulatory audit requirements

Is generative AI safe to use in banking given data privacy concerns?

Safety depends on deployment architecture. Banks can mitigate risk by running GenAI within their own secure AWS environment using services like Amazon Bedrock, where customer data isn't used to train models or shared externally. Strong access controls, encryption at rest and in transit, and audit logging complete the safeguard layer.

How can small and mid-sized banks get started with generative AI?

Start with one or two contained use cases — internal document summarization or fraud alert triage — rather than enterprise-wide rollouts. Use pre-built cloud AI services like AWS Bedrock rather than building models from scratch. Working with an AWS-certified implementation partner ensures compliant, cost-effective deployment without requiring a large internal AI team to manage it.