Introduction

Adding an AI chatbot to a fintech app is not a standard customer service bot deployment. The AI layer must connect securely to live financial data, satisfy regulatory requirements, and maintain user trust — all simultaneously. One misconfigured API permission or a compliance gap in your logging setup can create serious legal exposure.

According to the CFPB, approximately 98 million U.S. consumers interacted with a bank chatbot in 2022, with that figure projected to reach 110.9 million by 2026. The scale of adoption makes getting this right non-negotiable.

This guide covers the complete integration process: pre-build architecture decisions, tech stack selection, step-by-step setup, and post-integration compliance validation. It's written for teams with cloud infrastructure experience — ideally with NLP and API expertise — who need to deploy confidently.

Key Takeaways

- Compliance mapping and data governance must happen before any code is written

- Follow a fixed integration sequence: architecture, platform selection, API connectivity, NLP training, security hardening, then compliance validation

- AWS-native services (Lex, Bedrock, Lambda, API Gateway) provide a proven foundation for secure, scalable fintech chatbot deployments

- Post-integration testing must cover adversarial conversation scenarios and regulatory audit trail verification

- Skipping prerequisites doesn't save time; it creates costly rework after deployment

Prerequisites and Architecture Decisions for Fintech Chatbot Integration

Successful chatbot integration starts weeks before development. Teams must map which financial data the bot will access, define the permission model, and confirm data residency requirements — especially in regulated jurisdictions.

Prerequisites and Compliance Readiness

Before writing a single line of code, confirm the following:

Regulatory frameworks applicable to your deployment:

- PCI DSS v4.0.1 — applies if the chatbot stores, processes, or transmits cardholder data, or if middleware can affect the cardholder data environment (including Lambda functions, API Gateway configurations, and conversation logs)

- GDPR Article 5 / CCPA — require data minimization, storage limitation, and consumer rights handling for any chatbot logs containing user PII

- GDPR Article 22 — gives users rights around solely automated decisions with legal or significant effects; relevant if the chatbot contributes to credit decisions

- KYC/AML / FFIEC CIP — required for chatbot-assisted onboarding flows; FinCEN's 2024 alert specifically flags AI-generated identity artifacts as an evasion risk

Technical prerequisites that must exist before integration begins:

- Documented, secured backend APIs (undocumented APIs are a blocking dependency)

- An existing audit logging system that can be extended to chatbot interactions

- An authentication layer (OAuth 2.0, MFA) that can pass session context to chatbot sessions

- Legal sign-off on the scope of AI-driven financial guidance the bot is permitted to provide

Any gap in this list is a blocking issue — not a workaround to document and revisit after launch. Resolve these before architecture decisions begin.

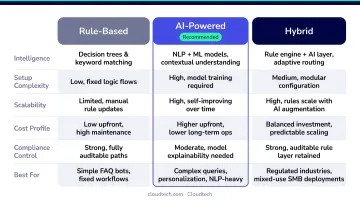

Chatbot Architecture: Rule-Based vs. AI-Powered vs. Hybrid

This architectural decision directly determines integration complexity:

| Architecture | Best For | Tradeoffs |

|---|---|---|

| Rule-based | Regulated transactional flows, compliance-sensitive paths | Fast to deploy, predictable outcomes, limited to defined decision trees |

| AI-powered | Conversational layers, multi-turn complex queries | Requires training data, ongoing model management, higher NLP risk |

| Hybrid | Most production fintech deployments | Rule-based for transactions, AI for conversation — balances compliance and flexibility |

Amazon Lex's Assisted NLU is a practical example of the hybrid model: it uses LLMs to improve intent classification and slot resolution while staying within configured intents and slots — keeping the AI layer constrained to what compliance teams have approved.

AWS Tech Stack for Fintech Chatbot Integration

The recommended AWS-native foundation:

- Amazon Lex V2 — NLP, intent recognition, ASR; AWS provides banking chatbot reference examples including balances, transfers, and transaction history

- AWS Lambda — serverless business logic execution; handles fulfillment behind each intent

- Amazon API Gateway — secure backend connectivity with rate limiting, Lambda authorizers, and access logging

- Amazon DynamoDB or ElastiCache — session state and conversation context persistence

- Amazon Bedrock — generative AI capabilities for complex, open-ended financial queries

- AWS CloudWatch + CloudTrail — structured logging, audit trail, and compliance monitoring

Additional dependencies: Plaid or Stripe APIs for account/transaction data, identity verification service connections, AES-256 encryption libraries, TLS 1.3 for data in transit.

Configuring this stack correctly in a regulated environment requires more than provisioning services — it requires knowing which defaults to override and which AWS controls satisfy specific compliance controls. Cloudtech's team, which includes former AWS engineers and a Principal Solutions Architect who has advised Capital One and other financial services firms, implements this foundation for fintech clients as part of its conversational AI practice.

How to Integrate an AI Chatbot into Your Fintech App: Step-by-Step

Fintech chatbot integration follows a strict sequence. Skipping ahead — deploying before security hardening or compliance validation — accounts for the majority of post-launch failures in this space. Each step below builds on the last.

Step 1: Define Conversation Scope and Intent Architecture

Document every financial task the chatbot will handle, then map each to a defined intent with example utterances.

For an initial deployment, limit scope to three to five high-frequency, low-risk intents:

- Balance inquiry

- Transaction status

- Transfer status

- Branch/service hours

- Basic account information

Each intent needs a minimum of 10 sample utterances per AWS Lex guidelines, with wide variety in phrasing. Keeping scope narrow reduces NLP training complexity and limits regulatory exposure during the learning phase.

Step 2: Connect the Chatbot to Financial Backend APIs

The chatbot connects to financial backends through a secure middleware layer ; AWS API Gateway combined with Lambda is the standard pattern.

Key requirements for this layer:

- Strict input validation on all parameters before they reach backend systems

- Configure rate limiting at API Gateway to prevent abuse

- Session-scoped access tokens (not persistent credentials)

- Lambda authorizers enforcing identity verification before any financial data is returned

Test every API endpoint in a sandbox environment before live connection. For Plaid integrations, use the sandbox environment to simulate account data responses. For Stripe, test PaymentIntent flows with test API keys before touching production credentials.

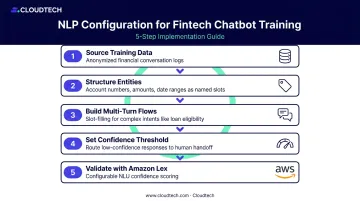

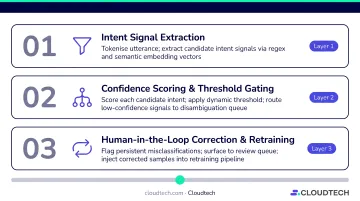

Step 3: Train and Configure the NLP Model on Financial Intents

Financial language is domain-specific. Users say "when will my transfer clear" , not "check transaction status." Training data must reflect how real users phrase financial questions.

NLP configuration requirements for fintech:

- Source training data from realistic financial conversation logs (anonymized and PII-scrubbed before use)

- Structure entities to capture account numbers, dollar amounts, date ranges, and transaction types as named slots

- Build multi-turn conversation flows for complex intents like loan eligibility , which require slot-filling (collecting required data points one at a time) across multiple exchanges

- Set a confidence threshold below which the bot defaults to human handoff instead of attempting a low-confidence response

- Amazon Lex provides configurable NLU confidence scoring built specifically for this purpose

Step 4: Implement Security and Authentication Handshake

The chatbot must never surface sensitive financial data (balances, transaction history, account numbers) until the user's session is authenticated.

Authentication requirements:

- The chatbot must inherit the user's authenticated state from the app's existing MFA or biometric flow

- Implement session context passing so the chatbot does not re-prompt for credentials mid-conversation

- Use Lex V2 session attributes to carry authentication state across conversation turns

- Store session tokens via AWS Secrets Manager , never hardcoded in Lambda environment variables

- Enforce minimum TLS 1.2 (TLS 1.3 recommended) for all API communications

Cloudtech's financial services security framework applies IAM least-privilege roles, short-lived session credentials, and AWS WAF at the API Gateway layer as standard controls for financial data access.

Step 5: Build the Human Handoff and Escalation Flow

Even a fully authenticated session will hit situations that require human judgment. Define trigger conditions that automatically transfer conversations to a live agent:

- High-value transactions above a defined threshold

- Fraud claims or suspected unauthorized activity

- Unrecognized intents after two retry loops

- Expressions of distress or urgency from the user

- Regulatory situations requiring human judgment

In regulated fintech environments, the handoff must preserve full conversation history and context. Agents need immediate access to what the chatbot already captured — repeating that intake process erodes trust and creates compliance gaps.

Post-Integration Testing and Compliance Validation

Fintech chatbot testing goes beyond standard QA. The bot is facilitating financial decisions, which means broken logic can cause incorrect account actions, data exposure, or regulatory violations. Testing must be completed and signed off before any production deployment.

Functional and Conversation Flow Testing

Scenarios that must be covered:

- Happy-path flows for every defined intent

- Edge cases: partial inputs, ambiguous queries, simultaneous sessions

- Multi-turn conversation integrity across session turns

- Correct slot-filling behavior (capturing required data fields) for complex intents

- Adversarial conversation testing — attempts to extract data or trigger actions outside the defined scope

Adversarial testing is non-negotiable. Cover prompt injection attempts, intent boundary violations, and data extraction through creative rephrasing — these are the failure modes regulators and auditors will ask about first.

Security and Data Exposure Testing

Use the OWASP API Security Top 10 (2023) as a testing framework for the chatbot-to-API layer. Priority test areas:

- Broken object-level authorization — can the chatbot access another user's account data?

- Authentication bypass — do bypass attempts fail cleanly?

- Rate limiting enforcement — does the API Gateway throttle as configured?

- Session expiry — does the chatbot correctly terminate sessions and refuse stale tokens?

- Log inspection — confirm no sensitive financial data (account numbers, balances) appears in conversation logs or error messages in plaintext

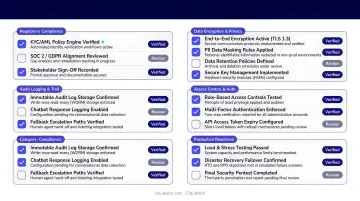

Compliance and Audit Trail Verification

Before go-live, verify:

- Every chatbot interaction is logged with: timestamp, user ID, intent triggered, data accessed, and outcome

- PCI DSS Requirement 10 controls are met for any interactions involving cardholder data

- GDPR Article 5 retention limits are applied to conversation logs containing PII

- Data retention policies are enforced — logs must not be stored indefinitely

- Credit-related or KYC flows can be explained and documented for regulators

Two regulatory obligations deserve separate attention:

- EU AI Act: Chatbots that support creditworthiness evaluation or credit scoring for EU users likely fall under the high-risk AI category, requiring transparency documentation and human oversight controls.

- CFPB guidance: Creditors using AI in credit decisions must provide specific, accurate adverse-action reasons — vague or model-generated explanations don't satisfy this requirement.

AWS CloudTrail and CloudWatch structured JSON logs handle this audit trail directly. Configure Lambda JSON logging before launch — it makes logs searchable and filterable across high log volumes and keeps your audit trail production-ready from the start.

Common AI Chatbot Integration Problems and Fixes

Most fintech chatbot integration failures fall into predictable categories. Knowing them in advance lets you build in safeguards before they become production issues.

Authentication and Session Continuity Failures

Problem: The chatbot loses the user's authenticated state mid-conversation, forcing re-authentication or surfacing an error instead of financial data.

Likely cause: Session tokens are not passed correctly through the API Gateway middleware, or token expiry intervals are too short for multi-turn financial conversations.

Fix: Use Lex V2 session attributes to persist authentication context across conversation turns. Align token expiry with realistic conversation duration — a loan application flow might take 8–12 turns. Store session state in DynamoDB for persistence across Lambda invocations.

NLP Misclassification of Financial Intents

Problem: The chatbot misroutes financial queries — treating "dispute a charge" as a general inquiry — leading to wrong responses or failed API calls.

Likely cause: Insufficient training data for domain-specific financial intents, or overlapping intent definitions that confuse the NLP model.

Fix: Address misclassification at three levels:

- Expand training utterances with diverse real-world phrasings for each financial intent

- Separate overlapping intents using distinct slot requirements

- Set a confidence threshold below which the bot routes to human handoff — Amazon Lex's configurable NLU confidence scoring handles this without custom code

Compliance Logging Gaps Discovered Post-Deployment

Problem: The integration passes functional testing but fails the compliance audit because chatbot logs are incomplete, lack user identifiers, or have no retention policy.

Likely cause: Logging was treated as a secondary concern and excluded from the integration architecture.

Fix: Build logging into the architecture from day one, not the audit:

- Implement AWS CloudWatch structured logging with JSON format at integration start

- Map each log field to its regulatory requirement — user ID for audit trail, timestamp for PCI Requirement 10, intent triggered for explainability

- Configure CloudWatch data retention policies before deployment, not after

Pro Tips for Successful AI Chatbot Integration in Fintech

Start narrow, expand deliberately. Deploy with three to five high-frequency, low-risk intents first. This limits regulatory exposure during the learning phase and lets the NLP model improve on real traffic before handling sensitive decisions like fraud disputes or loan applications.

Treat training data as a regulated asset. Financial conversation logs used for NLP training may contain PII. They must be anonymized, stored in compliant infrastructure, and governed under the same data policies as production financial data. This compliance gap often sits outside the app itself — and outside the scope of typical compliance reviews.

Plan for model drift from day one. Financial language, user behavior, and product offerings change over time, which degrades chatbot accuracy. Build a quarterly retraining schedule into the product roadmap and configure CloudWatch metrics to flag when intent recognition confidence scores drop below acceptable thresholds.

Know when outside expertise compresses the timeline. Fintech chatbot integrations involving core banking API connectivity, multi-region deployment, or complex compliance requirements are best handled by teams with prior experience in financial services architecture. Cloudtech's AWS-certified architects have built FINRA-compliant data pipelines and event-driven financial services architectures — work that helped one financial planning client avoid tens of millions in regulatory exposure — and apply that same hands-on experience to conversational AI engagements.

Frequently Asked Questions

How long does it take to integrate an AI chatbot into a fintech app?

A narrow-scope MVP integration covering three to five intents typically takes four to eight weeks. A full-featured deployment with complex flows, multi-region requirements, and compliance validation runs three to six months. Compliance readiness and backend API documentation are the biggest variables — teams with documented APIs and a clear regulatory baseline move significantly faster.

Can I add an AI chatbot to an existing fintech app without rebuilding the backend?

Yes. Integration is typically handled through an API middleware layer (API Gateway + Lambda) that connects the chatbot to existing backend services without restructuring the backend. The core requirement: well-documented, secured APIs and authentication tokens that pass through to chatbot sessions.

What AWS services are commonly used to build a fintech AI chatbot?

The core stack: Amazon Lex V2 for NLP and intent recognition, AWS Lambda for business logic, API Gateway for secure backend connectivity, Amazon Bedrock for generative AI capabilities, DynamoDB for session state, and CloudWatch + CloudTrail for compliance logging and audit trail.

What compliance requirements apply to AI chatbots in financial apps?

PCI DSS v4.0.1 applies when the chatbot handles cardholder data or can affect the cardholder data environment. GDPR and CCPA govern user data privacy and automated decision rights. KYC/AML and FFIEC CIP requirements apply to onboarding flows. The EU AI Act's high-risk classification applies to chatbots supporting creditworthiness or credit scoring decisions for EU users.

What is the difference between a rule-based and an AI-powered fintech chatbot?

Rule-based bots follow fixed decision trees, making them faster to deploy with more predictable compliance outcomes. AI-powered bots use NLP to handle varied natural language and complex multi-turn conversations, but require training data and ongoing model management. Most production fintech chatbots combine both: rule-based logic for regulated transactional flows, AI-powered NLP for the conversational layer.

How do I prevent my fintech chatbot from exposing sensitive financial data?

Three essential safeguards to implement:

- Enforce authenticated session inheritance before the chatbot accesses any financial data

- Restrict API permissions to the current intent so the chatbot can't request unrelated data

- Validate during testing that sensitive fields (account numbers, balances, SSNs) never appear in logs, error messages, or session stores in plaintext