This guide gives risk-aware mortgage lenders a practical view of where GenAI creates value, where it creates exposure, and what a structured risk management response looks like in practice.

Key Takeaways:

- GenAI automates high-friction mortgage processes, but each use case carries corresponding operational, compliance, and reputational risk

- Fraudsters are using GenAI to fabricate documents, build synthetic identities, and impersonate transaction parties

- Regulatory expectations are evolving fast — operating without a documented AI governance posture creates enforcement exposure

- A practical risk framework starts with knowing where AI lives — internally and across your vendor ecosystem

How GenAI Is Reshaping Mortgage Lending Operations

Traditional mortgage automation follows rules: if X, then Y. GenAI is different. It generates outputs — summaries, documents, risk assessments — based on what it was trained on. That distinction matters because it means greater capability alongside less predictable behavior than rule-based legacy systems.

Here's where lenders are deploying it today:

Loan Processing and Document Intelligence

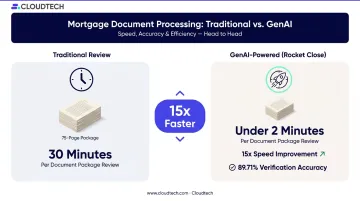

GenAI-powered tools extract, verify, and organize data from complex loan documents — pay stubs, bank statements, tax returns — at speeds that manual review cannot match. Rocket Close, using Amazon Textract and Amazon Bedrock on AWS, reduced abstract package processing from 30 minutes to under 2 minutes — a 15x speed improvement across 75-page packages at 89.71% verification accuracy. That's not a theoretical benchmark — it's a production result.

Credit Risk and Underwriting

GenAI enables underwriters to analyze larger, more varied borrower datasets — including alternative data sources like rent payment history and cash flow patterns. Fannie Mae found that 17% of applicants who received unfavorable Desktop Underwriter recommendations could have qualified if positive rent history had been considered. This expands credit access for underserved borrowers — but it also introduces fair lending risk that requires active management (addressed in the next section).

Compliance Automation and Fraud Detection

- Compliance: GenAI tools monitor regulatory changes in real time, map updates to internal policies, and draft required documentation — particularly valuable across RESPA, TILA, ECOA, and HMDA frameworks where a single missed update can create audit exposure

- Fraud detection: Lenders are deploying GenAI defensively to flag application anomalies, detect fraud patterns, and cross-reference transaction data at a scale manual review can't replicate

Borrower Experience

AI-powered assistants are reducing time spent on routine borrower inquiries and freeing loan officers for complex interactions. McKinsey documented a financial services company achieving a 25–30% reduction in contact center costs alongside a 5-percentage-point customer experience improvement through AI-enabled quality assurance — a model mortgage servicers are actively replicating.

The Internal Risk Landscape: What Mortgage Lenders Must Manage

Lenders adopting GenAI (whether building internally or through vendors) inherit a class of risks that traditional risk management programs weren't designed to handle. These aren't hypothetical concerns; they're already generating compliance issues at financial institutions.

Hallucinations and Inaccurate Outputs

GenAI models produce confident, plausible-sounding outputs that are sometimes factually wrong. In mortgage lending, that could mean an incorrect compliance summary, a flawed borrower-facing communication, or a miscalculated risk assessment. Without human review protocols, these errors reach borrowers or regulators before anyone catches them.

Algorithmic Bias and Fair Lending Exposure

Models trained on historical lending data can inherit and amplify existing biases , producing disparate impact on protected class borrowers under ECOA and the Fair Housing Act. Lenders are legally accountable for every lending decision, regardless of whether an AI model drove it.

Minimum bias audit practices include:

- Diverse training datasets that reflect the full borrower population

- Regular fairness assessments measuring outcome disparities by protected class

- Adverse action notices that provide specific, explainable reasons — model complexity does not satisfy Regulation B's requirements under 12 CFR 1002.9

Third-Party and Vendor AI Risk

Your AI risk posture extends to every vendor using GenAI on your behalf , yet many lenders don't know which technology partners have quietly introduced GenAI into their workflows. Minimum controls include AI-specific contract language, vendor due diligence questionnaires, and disclosure requirements.

"Shadow AI" compounds this problem: employees using unapproved consumer tools like ChatGPT or Gemini to process loan data. The result is data exposure and audit trail gaps that are difficult to detect and nearly impossible to reconstruct.

Data Privacy and Security Exposure

Those same vendor access points create direct data exposure risk. GenAI systems require high data volume to operate, and in mortgage lending that data is highly sensitive: SSNs, financial histories, property records.

The FTC Safeguards Rule applies directly to mortgage lenders and brokers, requiring:

- Written information security programs and risk assessments

- Encryption and access controls

- Contractual safeguard requirements for service providers

Data flowing through third-party GenAI platforms may not meet those standards by default.

Black Box Decision-Making

When a GenAI model cannot explain how it reached a conclusion, you have both a compliance risk and a governance problem. Explainable AI (XAI) capability should be a procurement criterion when evaluating any GenAI vendor whose tools will touch credit decisions, pricing, or adverse action workflows.

AI-Driven Fraud: The External Threat Targeting Mortgage Lenders

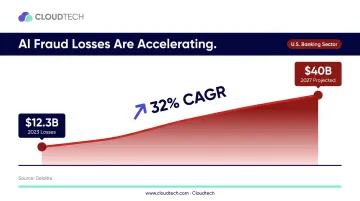

AI is not only a tool lenders deploy — it's a weapon fraudsters are deploying against lenders. Deloitte forecasts that U.S. generative AI-enabled banking fraud losses will grow from $12.3 billion in 2023 to $40 billion by 2027 — a 32% compound annual growth rate. The detection capabilities at many institutions have not kept pace.

Synthetic Identities and AI-Fabricated Documents

Synthetic identity fraud combines real data points from multiple individuals into a single convincing persona. These identities can pass standard verification checks, accumulate credit history, and eventually land a fraudulent mortgage loan — with no single real victim triggering a fraud alert.

GenAI has sharpened this threat considerably. Modern tools produce authentic-looking pay stubs, W-2s, bank statements, and tax returns that clear visual inspection without issue. Lenders relying solely on document review — rather than source verification — face substantial exposure that didn't exist five years ago.

Deepfakes in Transaction Impersonation

FinCEN's 2024 alert documented rising suspicious activity involving deepfakes used to impersonate account holders and authorize transactions. In mortgage contexts specifically, fraudsters clone audio from LinkedIn profiles or voicemail recordings to mimic transaction participants during verification calls — redirecting wire transfers or altering closing instructions.

Verbal verification alone is no longer a reliable control. Lenders need layered identity checks at every high-stakes transaction point.

Countermeasures: Updated Detection and Verification

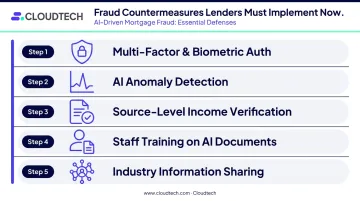

Practical steps lenders should implement:

- Deploy multi-factor authentication and biometric verification at key transaction points, not just at login

- Implement AI-powered anomaly detection to flag application patterns inconsistent with legitimate borrowers

- Verify income and employment at the source — document review alone no longer constitutes sufficient due diligence

- Train staff to recognize AI-generated document characteristics; Fannie Mae's fraud prevention materials flag inconsistent pay stubs, unexplained deposits, and identity discrepancies as file-level indicators

- Participate in industry information-sharing networks — FinCEN's deepfake alert (FIN-2024-Alert004) recommends SAR filings referencing FIN-2024-DEEPFAKE for relevant suspicious activity

The Evolving Regulatory Landscape for GenAI in Mortgage Lending

As of 2026, no federal agency has issued a comprehensive GenAI governance framework specific to mortgage lenders. But the direction of regulatory expectations is clear.

The OCC, Federal Reserve, and FDIC issued revised model risk guidance on April 17, 2026 (SR 26-2 / OCC Bulletin 2026-13). Notably, generative and agentic AI were explicitly placed outside that guidance's scope: regulators acknowledged these technologies present distinct risks requiring a separate governance approach still under development.

The guidance applies most directly to banking organizations over $30 billion in total assets, though its principles signal broader expectations for the industry as a whole.

Fair Lending and Adverse Action Obligations

ECOA and the Fair Housing Act apply regardless of whether lending decisions are made by humans or AI models. Regulation B still requires adverse action notices with specific principal reasons. Model complexity is not an acceptable substitute.

Two regulatory developments are reshaping this terrain, but neither eliminates core obligations:

- CFPB's April 2026 final rule narrows ECOA disparate-impact liability (effective July 21, 2026)

- HUD's proposed rule revisits disparate-impact regulations

Intentional discrimination and proxy-based discrimination remain prohibited under any regulatory scenario. These developments do not reduce fair lending scrutiny.

AI Washing and Disclosure Risk

The SEC's 2024 enforcement actions against investment advisers are a direct signal for mortgage lenders: Delphia received a $225,000 penalty and Global Predictions a $175,000 penalty, both for making false claims about AI capabilities. Regulatory agencies are watching how institutions represent their AI use.

Any claim about GenAI capabilities — internal or external — must be accurate and documented before it reaches examiners. Independent verification is not optional.

A Practical GenAI Risk Management Framework for Mortgage Lenders

Effective GenAI risk management is an ongoing program, not a one-time project. It requires visibility, governance, and human oversight — and lenders who treat it purely as a technology implementation tend to encounter the same gaps that have produced costly enforcement actions and fraud losses at peer institutions.

Build an AI Inventory and Govern Vendor AI

Start here. You cannot manage risk you haven't mapped.

An AI inventory should capture:

- Which internal workflows use AI, which models, and what data they process

- Which vendors use GenAI, how, and under what contractual controls

- Where shadow AI is likely in use and how to bring it into governance scope

This inventory becomes the foundation for risk assessment, policy development, and examiner-ready documentation.

For lenders deploying GenAI on cloud infrastructure, the underlying environment must meet the security, access control, and auditability standards regulators require. Cloudtech supports financial services clients in configuring AWS infrastructure to those standards — including encryption at rest and in transit, IAM-based access controls, CloudTrail audit logging, and compliance monitoring through Amazon GuardDuty and AWS Security Hub.

Apply the Risk Lifecycle to GenAI

Standard risk management steps apply directly — they just need to be applied more frequently than traditional model risk processes:

- Identify: Where is AI in use, internally and externally? What could go wrong with each use case?

- Assess: What is the inherent risk? What controls currently exist? What are the gaps?

- Treat: Decide to avoid, mitigate, transfer, or accept based on your documented risk appetite

- Monitor: Continuously review AI outputs, vendor disclosures, model performance, and regulatory developments

GenAI risk assessments should be revisited more frequently than traditional model risk reviews — the technology, its use cases, and its threat landscape are all evolving rapidly.

Human Oversight, Explainability, and Culture

No GenAI risk framework is complete without three non-negotiable elements:

- Human-in-the-loop requirements for high-stakes decisions: loan approvals, adverse actions, fraud flags

- Bias auditing and explainability standards for any model used in credit decisions or pricing

- Staff training that builds awareness of responsible GenAI use and creates clear escalation paths for concerns

Lenders are legally and regulatorily responsible for all lending decisions. AI does not transfer accountability — it creates new obligations to demonstrate that accountability is being exercised.

Frequently Asked Questions

What is generative AI, and how does it differ from other types of AI used in mortgage lending?

GenAI generates new outputs — text, documents, summaries — based on training data, while predictive AI forecasts outcomes like default probability based on input variables. Each has a distinct risk and compliance profile: predictive models carry well-understood model risk, while GenAI introduces hallucination risk, data privacy exposure, and greater explainability challenges.

What are the biggest risks of using generative AI in mortgage lending?

The primary internal risks are hallucinated outputs, algorithmic bias creating fair lending exposure, data privacy vulnerabilities, and third-party/vendor AI risk. All four require active, ongoing governance, not a one-time setup.

How are fraudsters using AI to target mortgage lenders?

Three primary attack vectors have emerged: synthetic identity creation (combining real data into convincing fake borrowers), AI-fabricated financial documents that pass visual inspection, and deepfake voice or video used to impersonate transaction parties. Traditional document review and verbal verification are no longer sufficient controls on their own.

Does using AI in mortgage underwriting create fair lending liability?

Yes. ECOA and the Fair Housing Act apply regardless of whether decisions are AI-driven. Lenders must explain adverse actions with specific reasons and demonstrate their models don't produce disparate impact on protected classes. Bias auditing is a regulatory expectation, not an optional practice.

What does current regulatory guidance say about GenAI in mortgage lending?

As of mid-2026, comprehensive GenAI-specific regulation for mortgage lenders is still developing. Existing fair lending, data privacy, and model risk obligations apply now. The April 2026 interagency model risk guidance explicitly excluded GenAI from scope, signaling that regulators view it as requiring distinct treatment not yet finalized.

How should a mortgage lender get started with GenAI risk management?

Build an AI inventory covering internal use and vendor use, define a risk appetite for AI, and establish human review requirements for high-stakes AI-assisted decisions. These three steps are the foundation — everything else builds from knowing where AI lives and who's accountable for its outputs.