Introduction

Mortgage applications are among the most document-heavy transactions in financial services. Borrowers hand over tax returns, pay stubs, W-2s, bank statements, and credit histories — a full financial profile that represents both significant personal trust and serious security liability.

That combination makes mortgage lenders cautious about AI adoption. According to a Fannie Mae survey of 219 lending institutions, only 7% of lenders were broadly using AI or ML in Q3 2023, with 22% in limited trials and 41% still investigating. The hesitation isn't about doubting AI's potential — it's about managing the risk that comes with deploying it incorrectly.

Lenders that deploy generative AI securely can cut origination costs, accelerate underwriting, and deliver a better borrower experience — while those still waiting face a narrowing window before early adopters lock in a structural advantage.

This article covers:

- Where GenAI adds real value across the mortgage lifecycle

- What "secure by design" actually means in practice

- How to stay on the right side of CFPB and GLBA requirements

- What a compliant AWS-based architecture looks like for SMB mortgage lenders

Key Takeaways

- Average origination costs reached $11,600 per loan in Q3 2023 — GenAI addresses the manual processing that drives this figure

- RAG architectures limit data exposure by retrieving only relevant context, not full borrower files

- CFPB, HUD, and GLBA regulations apply equally to AI-driven decisions — no exemptions exist

- Amazon Bedrock allows private model deployment where borrower data is never used for third-party model training

- An experienced AWS partner can deploy secure GenAI infrastructure in weeks, not months built from scratch

Why Mortgage Lenders Are Turning to Generative AI

The Cost Pressure Is Real

Freddie Mac's 2024 Cost to Originate Study puts average origination costs at approximately $11,600 per loan in Q3 2023 — up roughly 35% over three years. Personnel accounts for 67% of production expense. The gap between the most and least efficient lenders is stark: the top quartile averages $6,900 per loan versus $16,500 for the bottom quartile.

The same study found that heavy users of digital tools had costs approximately $1,500 (14%) lower and production cycles five days shorter. Lenders who responded to the survey believed a fully digital process could cut costs by as much as 40%.

That's the operational pressure driving GenAI interest. Lenders recognize the efficiency gap — and many are looking at generative AI to close it.

GenAI vs. Traditional Automation

Rules-based tools like Fannie Mae's Desktop Underwriter or standard OCR platforms execute predefined logic. They're fast within their defined scope but can't reason across documents, handle ambiguous data, or generate context-aware responses.

Generative AI does something different:

- Reads and reasons across unstructured documents — appraisal reports, income narratives, title exceptions

- Generates explanations rather than just outputting a pass/fail score

- Adapts responses based on the specific borrower context, not a generic template

- Synthesizes information from multiple documents simultaneously

Why Adoption Has Lagged

Despite those advantages, GenAI adoption in mortgage lending has moved slowly. The Fannie Mae survey identified the top barriers: integration with existing infrastructure (48%), lack of a proven success record (35%), and cost (24%). Underneath those stated concerns are deeper anxieties — hallucinated financial calculations, bias in credit decisions, and regulatory exposure.

Solving the security and governance layer is what turns those concerns into a manageable checklist rather than a dealbreaker.

Key GenAI Use Cases Across the Mortgage Lifecycle

GenAI's impact isn't limited to one stage. It applies from initial borrower inquiry through loan servicing and default management.

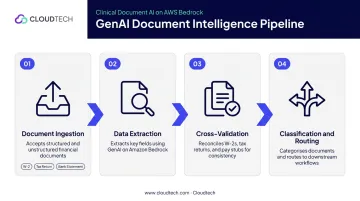

Loan Origination and Document Intelligence

The origination process is document-intensive by nature. A typical mortgage file includes dozens of pages across pay stubs, W-2s, bank statements, tax returns, and employment verification letters — each requiring extraction, validation, and cross-referencing.

GenAI-powered document intelligence automates that process:

- Extracts structured data from unstructured documents without manual data entry

- Cross-validates income figures across W-2s, tax returns, and pay stubs automatically

- Flags inconsistencies that would take a loan officer hours to catch manually

- Classifies documents on ingestion, routing them to the correct workflow

Cloudtech's Intelligent Document Processing pipeline — built on Amazon Textract, AWS Lambda, and Amazon S3 — handles these workflows for financial clients, with Amazon Textract explicitly supporting lending document types. This cuts processing time and reduces errors that manual review tends to introduce.

Document intelligence is only part of the origination picture. GenAI-powered chatbots can also guide borrowers through product selection and initiate the 1003 application process without a human agent at every step.

Mortgage Servicing and Borrower Support

Servicing teams handle thousands of borrower inquiries monthly: payment status questions, escrow adjustments, forbearance eligibility, loss mitigation options. Handling these at scale with human agents is expensive and inconsistent.

Large language models deployed with Retrieval-Augmented Generation (RAG) architectures can serve as virtual loan assistants, answering borrower questions by retrieving information only from the servicer's own approved policy documents. This keeps responses within regulatory and policy boundaries, rather than generating plausible-sounding but incorrect answers.

The same approach improves internal servicing team productivity:

- Transcribes and summarizes call notes automatically

- Categorizes borrower complaints for routing and reporting

- Surfaces relevant regulatory guidance from dense servicing handbooks on demand

MBA's Servicing Operations Study reported the average annual cost to service a non-performing loan at $1,857 versus $176 for a performing loan in 2023. Tools that help servicers identify and reach at-risk borrowers earlier directly affect which category those loans end up in.

Risk, Fraud Detection, and Underwriting Support

Cotality's 2025 Annual Fraud Report found that 0.86% of applications — roughly 1 in 116 — showed fraud indicators in Q2 2025, up from 1 in 123 a year earlier. Purchase applications carried even higher risk at approximately 1 in 106.

Machine learning models detect anomalies in application data (income inconsistencies, address mismatches, unusual transaction patterns) that manual review misses. GenAI adds a layer on top:

- Generates narrative summaries of anomaly findings for underwriters

- Surfaces relevant fraud typologies from regulatory guidance

- Flags early default risk signals before delinquency escalates

The Security Challenge: Why "Secure by Design" Matters for Mortgage AI

Why Mortgage Data Is a High-Value Target

A mortgage application contains nearly everything needed for identity theft: Social Security numbers, tax IDs, bank account numbers, employment history, and complete financial profiles. A GenAI deployment that isn't properly architected can expose this data through model training leakage, insecure API calls, or misconfigured storage.

The risk isn't hypothetical. A 2025 multistate regulatory action required Bayview Asset Management to pay $20 million after a breach affecting 5.8 million customers, citing deficient cybersecurity practices. IBM's 2024 breach cost study puts the average financial-sector breach at $6.08 million — nearly $1.2 million above the cross-industry average.

The Public AI Model Problem

Submitting borrower data to general-purpose AI APIs without proper isolation creates a specific risk: some providers use customer inputs to improve their models. That creates a data privacy obligation under GLBA — and potentially under state-level privacy laws — that most lenders haven't fully thought through.

The FTC's amended GLBA Safeguards Rule (effective June 2023) sets clear expectations for covered financial institutions:

- Encrypt customer information at rest and in transit

- Control and periodically review access permissions

- Require multi-factor authentication (MFA)

- Monitor and log authorized-user activity

- Maintain documented incident-response plans

Secure by Design: The Core Principles

A properly architected mortgage GenAI deployment includes:

- Data encryption at rest and in transit using customer-managed keys

- Strict IAM policies ensuring only authorized users can query sensitive borrower data

- Private network isolation (VPC) preventing data from traversing public infrastructure

- Audit logging for every AI interaction involving borrower data

- RAG-based retrieval that limits data exposure to only the context needed for a specific query

RAG architecture is worth unpacking here. The foundation model never receives the full borrower file — only the relevant document excerpts needed to answer a specific question. This limits exposure at the model level while preserving accuracy, which matters when regulators ask how your AI handles NPI.

Human-in-the-Loop for High-Stakes Decisions

GenAI should augment human judgment, not replace it at regulated decision points. In mortgage lending, that means human review is non-negotiable for:

- Loan approvals and adverse action notices

- Denial reason documentation (ECOA/Reg B requirements)

- Loss mitigation recommendations

Model output monitoring and human-in-the-loop workflows aren't just best practice — in regulated environments, they're a compliance requirement. Designing those checkpoints into the architecture from day one is far easier than retrofitting them later.

Staying Compliant: Managing Regulatory and Ethical AI Risks

The Regulatory Framework

No special exemption exists for AI. Lenders remain responsible for every decision their systems make. The key frameworks:

- CFPB Circular 2023-03: Creditors using AI must provide specific, accurate reasons for adverse action. Model opacity isn't an excuse — sample-form denial reasons that don't reflect the actual model output violate the circular.

- HUD Fair Housing Act guidance (May 2024): The Fair Housing Act applies when AI or algorithms are used to target and deliver housing-related advertisements. Directing protected groups toward predatory products or denying them housing information constitutes a potential violation.

- GLBA: Data protection obligations apply regardless of whether AI is processing the data.

Algorithmic Bias

AI models trained on historical mortgage data can replicate historical lending disparities. Peer-reviewed research found that Latinx and Black borrowers paid 7.9 basis points more for purchase mortgages after controlling for observed risk factors, with FinTech lenders reducing but not eliminating those disparities.

Mitigating bias requires:

- Diverse and representative training datasets

- Regular bias audits with documented methodology

- Explainable AI outputs that compliance teams can actually review

- GenAI partners who build fairness testing into their development process

Human-in-the-Loop as Compliance Infrastructure

GenAI can process, recommend, and summarize. Final lending decisions must involve human review. Any adverse action that triggers regulatory notification requirements demands documented human sign-off before it goes out. Regulators have been explicit on this point.

In practice, that means structuring your AI workflows so that:

- A licensed underwriter reviews and approves all credit decisions

- Adverse action notices reflect the actual model output, not generic templates

- Human review is logged and auditable for examination purposes

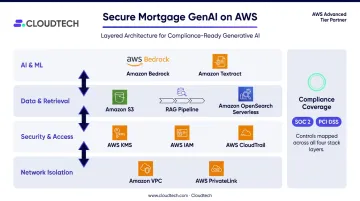

Building Secure GenAI on AWS: What the Right Infrastructure Looks Like

Why AWS for Mortgage GenAI

AWS provides purpose-built security services that align directly with GLBA, SOC 2, and financial services security requirements. **Amazon Bedrock does not use customer prompts or outputs to train AWS models**, and model providers don't receive access to those inputs and outputs. AWS PrivateLink connects a VPC privately to Bedrock without exposing traffic to the public internet.

The core services in scope for SOC and PCI compliance programs:

| AWS Service | SOC Scope | PCI Scope |

|---|---|---|

| Amazon Bedrock | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

| AWS KMS | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

| AWS IAM | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

| AWS CloudTrail | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

| Amazon VPC | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

| Amazon S3 | SOC 1, 2, and 3 | PCI DSS and PCI 3DS |

Note: Listing a service in an AWS assurance program certifies the service, not the lender's workload. Correct configuration is the lender's responsibility.

The Architecture Components

A secure mortgage GenAI stack on AWS includes:

- Amazon Bedrock for private foundation model deployment

- Encrypted S3 buckets with strict bucket policies for borrower document storage

- RAG pipeline using Bedrock Knowledge Bases and OpenSearch Serverless for vector search and retrieval

- Amazon Textract for document extraction across lending document types

- AWS CloudTrail for complete audit logging of AI interactions

- Amazon VPC with PrivateLink to keep all traffic off the public internet

- AWS KMS for encryption key management with customer-managed keys

- AWS IAM with least-privilege policies and regular access reviews

Why Pre-Built Beats Starting from Scratch

Each component in that stack is only as secure as its configuration. The most common mortgage AI deployment failures come down to configuration errors — overly permissive IAM roles, publicly exposed S3 buckets, and API Gateway endpoints missing proper authentication are recurring problems in financial services cloud environments.

Cloudtech's team — with 70% former AWS employees and 100+ AWS certifications — has documented and corrected each of these failure patterns in SMB financial services environments. Their approach embeds security guardrails during the discovery phase rather than remediating after an audit finding.

For SMB mortgage lenders, the practical benefit is access to the same security architecture used by large financial institutions — without needing an in-house AWS team to configure it correctly. Cloudtech's engagement structure is built for that reality:

- IDP solution: $7,999 as a one-time deployment

- GenAI on Bedrock: Fixed-fee 4–8 week pilot POC before any full production commitment

- AWS Partner Funding: May offset a portion of engagement costs for qualifying workloads

Frequently Asked Questions

How is AI being used in the mortgage industry?

AI is applied across the full loan lifecycle: document extraction and data validation during origination, AI-powered chatbots for borrower self-service, fraud detection and anomaly flagging in underwriting, and predictive analytics for early default identification in servicing. Most lenders start with one or two high-value use cases — document extraction or borrower self-service — before expanding further.

Will mortgage loan officers be replaced by AI?

No. AI handles repetitive data tasks — document extraction, data validation, inquiry routing — so loan officers can focus on borrower relationships, complex cases, and judgment-dependent decisions. Regulated lending decisions also require human review by law, which keeps MLOs central to the process.

What makes generative AI "secure" for handling sensitive mortgage data?

Secure mortgage GenAI requires private model deployment, encryption at rest and in transit, strict IAM access controls, VPC network isolation, and complete audit logging — ensuring no borrower data reaches third-party training pipelines. RAG architectures further restrict model access to only the data relevant to each specific query.

How does generative AI help mortgage lenders stay compliant?

GenAI can automate compliance checks, monitor for regulatory updates, and generate explainable outputs — but human oversight is required. The underlying governance framework must satisfy CFPB adverse action rules, HUD Fair Housing guidance, and GLBA data protection obligations.

What is RAG and why does it matter for mortgage AI?

Retrieval-Augmented Generation allows AI to answer questions by pulling information only from pre-approved sources — servicer policy documents, regulatory guides, approved FAQ content — rather than relying on general training data. This reduces hallucinations and keeps responses within regulatory boundaries, which is critical when AI touches borrower communications or compliance workflows.

How long does it take for a mortgage lender to implement a secure GenAI solution?

With a pre-configured AWS-based approach, foundational GenAI capabilities can be operational in weeks rather than months. Cloudtech's model begins with a fixed-fee 4-8 week pilot POC to validate a specific use case, then moves to production build — faster than building security controls, RAG pipelines, and compliance guardrails independently from the ground up.