Generative AI is a direct response to that pressure. Not as a vague technology trend, but as a practical tool showing up in specific workflows: faster fraud detection, automated compliance documentation, AI-powered customer support that doesn't require a human for every interaction.

This article explains what generative AI actually does in fintech, where it delivers the most measurable impact, and what financial services teams can do to act on it — without building custom models from scratch.

Key Takeaways

- Generative AI uses large language models to generate reports, summaries, and responses from unstructured financial data

- Highest-impact applications: fraud detection, AI-powered customer support, KYC/AML document processing, and compliance reporting

- The generative AI in fintech market is valued at $2.17 billion in 2025, growing at 35.3% CAGR

- Benefits are measurable: lower fraud loss rates, reduced compliance overhead, faster customer resolution

- AWS Bedrock and similar cloud tools make adoption accessible for SMBs — no custom model development required

What Is Generative AI in Fintech?

Generative AI is a category of AI that creates new outputs — text, synthetic data, reports, code — by learning patterns from large datasets. Unlike traditional rule-based systems that follow fixed logic, or predictive ML models that classify structured data, generative AI interprets context and generates responses.

In practice, it can read a contract, summarize its key terms, flag anomalies, and produce a compliance-ready report draft with no manual data entry required.

The U.S. Treasury defines it as AI that "can create new content based on what it learns from training data," distinguishing it from earlier AI that simply applied fixed rules to structured inputs.

In fintech specifically, generative AI works best on text-heavy, unstructured, and workflow-intensive processes: document review, customer communication, regulatory reporting, and fraud narrative analysis. It's not replacing core financial systems — it's an augmentation layer that cuts the manual hours that document-heavy workflows have always demanded.

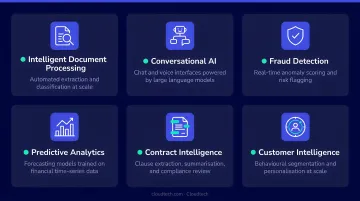

Key Application Areas

Fintech teams are actively deploying generative AI across six primary areas:

- Fraud detection and anomaly identification — real-time pattern analysis across transaction data

- AI-powered customer support — LLM-driven chatbots handling account queries, disputes, and financial guidance

- KYC/AML document processing — automated extraction and review of identity and compliance documents

- Credit risk assessment — AI-generated summaries and scoring inputs from unstructured applicant data

- Compliance report generation — automated drafting of regulatory filings and suspicious activity reports

- Algorithmic trading support — market signal analysis and trade narrative generation

Adoption across these areas is accelerating fast. According to The Business Research Company, the generative AI in fintech sector is forecast to reach $9.76 billion by 2030, growing at a sustained 35% CAGR.

Key Benefits of Generative AI in Fintech

The benefits below connect directly to KPIs that fintech teams track: fraud loss rates, cost per transaction, customer resolution time, and compliance overhead. Each one is operational and measurable.

Benefit 1: Faster, More Accurate Fraud Detection

Traditional fraud detection depends on predefined rules. Fraudsters learn those rules and adapt. Generative AI doesn't rely on static thresholds — it analyzes behavioral patterns, transaction context, and historical signals simultaneously to identify anomalies that rule-based systems miss entirely.

Mastercard's generative AI fraud technology doubled the speed of compromised card detection, improved fraud identification by an average of 20% (up to 300% in specific cases), and reduced false positives by up to 200%.

That last figure matters as much as detection accuracy — high false positive rates create their own operational burden, triggering unnecessary investigations and degrading customer experience.

Gen AI also addresses the data scarcity problem in fraud model training. By generating synthetic transaction data, it enables detection models to train on realistic fraud scenarios without exposing real customer records — a critical advantage for regulated environments.

KPIs directly impacted:

- Fraud loss rate

- False positive rate in transaction monitoring

- Time-to-detect and time-to-flag mid-transaction

- AML case resolution time

- Operational cost of fraud investigation teams

This benefit is most valuable for high transaction volume environments, companies processing payments across multiple geographies, and any firm facing regulatory scrutiny for AML/KYC compliance.

For context: the FBI IC3 reported suspected internet-crime losses exceeding $16 billion in 2024, up 33% from the prior year — and financial-crime compliance costs in the U.S. and Canada already total $61 billion annually according to LexisNexis Risk Solutions.

Benefit 2: Personalized Customer Experiences at Scale

Personalized financial guidance was previously only possible if you had a large enough service team to support it. Generative AI changes that equation, allowing fintech platforms to deliver individualized support — powered by each user's transaction history, goals, and behavior — without routing every interaction through a human advisor.

In practice, this means:

- LLM-powered chatbots that handle account queries, dispute status, and budgeting questions contextually rather than from rigid scripts

- AI-generated financial summaries tailored to individual spending patterns

- Adaptive onboarding flows that respond to user inputs conversationally

- Product recommendations triggered by specific behavioral signals

The satisfaction impact is real. J.D. Power data shows that virtual assistant users in banking and credit card mobile apps score 18 points higher in overall satisfaction than non-users — a material difference in an industry where 13% of U.S. retail banking customers were likely to switch institutions within 12 months as of 2024.

KPIs directly impacted:

- Customer satisfaction score (CSAT/NPS)

- First-contact resolution rate

- Support cost per interaction

- Product cross-sell rate

- Onboarding completion rate

This matters most for fintech platforms with high user volumes and thin support teams — and for any company competing with larger banks on experience quality rather than product breadth.

Benefit 3: Operational Efficiency and Cost Reduction

Compliance documentation, KYC document review, financial statement summarization, dispute resolution write-ups — these workflows are not just time-consuming, they introduce inconsistency and error when processed manually at scale.

McKinsey estimates generative AI could add $200 billion to $340 billion in annual value to global banking — equal to 9% to 15% of operating profits. A concrete example from their research: one bank reduced investment brief production time by more than 90%, from nine hours to 30 minutes, using generative AI.

Accenture puts the scale of the opportunity in sharper terms: 73% of U.S. bank employee time has high potential to be affected by generative AI, split between 39% with automation potential and 34% with augmentation potential.

For fintech SMBs, this creates a critical advantage. Manual processing of compliance reports, onboarding documents, and customer communications creates a growth ceiling — scaling means proportionally scaling headcount. Generative AI breaks that relationship.

KPIs directly impacted:

- Cost per compliance report

- Document processing time and error rate

- Headcount required for back-office operations

- Time-to-onboard new customers

Cloudtech's intelligent document processing platform — built on Amazon Textract and Amazon Q Business — directly targets this problem. It automates the extraction of structured data from unstructured documents (contracts, financial filings, compliance records), connects outputs to natural language interfaces, and deploys inside the client's own AWS environment.

For financial services SMBs, this means no data on third-party infrastructure and compliance controls that meet the requirements of regulated workloads.

What Happens When Fintech Companies Ignore Generative AI

The cost of delay isn't just a missed efficiency opportunity — it's compounding.

Deloitte reports that 46% of financial services respondents now qualify as generative AI "pioneers," with 76% allocating 20% or more of their AI budgets to it. The gap between early adopters and laggards is no longer theoretical — it shows up in fraud losses, churn rates, and compliance overhead.

Here's where the damage accumulates:

- Fraud detection falls further behind. As transaction volume grows, human-only review teams can't keep pace. Novel fraud patterns go undetected longer, loss ratios climb, and regulatory exposure increases.

- Customer experience degrades. Competitors deploying AI-powered support deliver faster onboarding and more responsive service. PwC data shows 29% of consumers abandoned a brand due to poor experience — a real risk when switching friction is low.

- Compliance costs don't plateau. LexisNexis Risk Solutions found 99% of U.S. and Canadian financial institutions reported rising compliance costs. Without AI-assisted document review and reporting, error rates stay elevated and audit exposure grows.

- Scaling requires more headcount, not smarter systems. Every growth milestone triggers proportional staff additions in fraud ops, compliance, and support — a model that puts SMBs and fintech startups at a structural disadvantage against larger institutions that have already automated these functions.

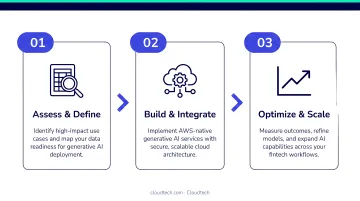

How to Get the Most Value from Generative AI in Fintech

Generative AI delivers the highest ROI when applied to specific, well-defined workflows first — not broad "AI transformation" initiatives.

Start with your highest-volume, most manual processes. The clearest starting points are workflows with unstructured data, tight compliance timelines, or repetitive human review. Common first deployments: compliance report drafting, KYC document extraction, and customer support automation.

Build feedback loops from day one. AI-generated fraud alerts need clear escalation paths. Compliance reports need human sign-off workflows. Customer interactions need feedback mechanisms so models improve over time. Value compounds when outputs are actually acted upon — not when AI runs in isolation.

Treat infrastructure as a first-order concern. Generative AI in fintech runs on cloud infrastructure, and the quality of that foundation determines the reliability of every AI output. For regulated workloads, security, latency, data residency, and compliance controls aren't optional — they're baseline requirements.

That infrastructure foundation is where many fintech SMBs and startups get stuck. Cloudtech, an AWS Advanced Tier Partner, helps financial services teams build that foundation without diverting engineering resources from core product work. The engagement starts with an assessment of existing data — volume, access patterns, growth trajectory — then builds the automated pipelines and AI-ready data layer that generative AI applications require.

Deployments happen inside the client's own AWS environment, keeping data in-house and compliance controls where they belong: with the client.

A focused engagement — Cloudtech offers 10-hour AWS-Certified Solutions Architect consultations as an entry point — can help fintech teams identify their highest-impact starting workflow before committing to a full implementation.

Conclusion

Generative AI's value in fintech is not theoretical. It shows up as faster fraud detection, lower compliance overhead, and customer experiences that previously required far more human involvement. The Mastercard fraud results, McKinsey's banking efficiency benchmarks, and J.D. Power's virtual assistant satisfaction data all point in the same direction: this is where operational improvement is already measurable.

The advantages compound over time:

- Models improve as they process more data

- Automation removes the manual bottlenecks that constrain growth

- Personalized experiences drive retention and reduce acquisition cost

Financial services companies that build generative AI into core operations now will have a widening advantage over those still relying on manual processes. The operational gap between them and their competitors is already growing.

Frequently Asked Questions

How is generative AI being used in fintech?

Generative AI is applied across fraud detection, automated KYC/AML document review, AI-powered customer support chatbots, credit risk assessment, compliance report generation, and personalized financial recommendations. Fraud monitoring and compliance automation represent the most mature deployments, driven by the sheer volume of unstructured data involved.

What is the difference between generative AI and traditional AI in fintech?

Traditional AI — including rule-based systems and predictive ML — analyzes structured data to make predictions or trigger actions. Generative AI creates new outputs (reports, summaries, responses) from unstructured data like documents and conversations. In practice, most fintech operations need both — but generative AI handles the document-heavy, text-driven workflows that traditional ML simply wasn't built for.

Can small fintech companies and SMBs afford to adopt generative AI?

Yes. Cloud-based services like AWS Bedrock use pay-as-you-go pricing, so there's no need to build or train custom models. Starting with a single use case — customer support or compliance reporting — keeps costs manageable and builds a clear ROI case before expanding.

How does generative AI improve regulatory compliance in fintech?

Gen AI automates the drafting of compliance reports, extracts and flags relevant data from regulatory documents, monitors for policy changes, and maintains audit-ready records. This reduces both the time and error rate associated with manual compliance workflows — directly lowering audit exposure.

What are the biggest risks of using generative AI in financial services?

The primary risks are data privacy exposure, model bias in credit or fraud decisions, hallucinations (plausible but inaccurate outputs), and compliance gaps. FINRA, the FSB, and the U.S. Treasury each flag these concerns — addressing them requires human oversight, strong data governance, and infrastructure designed for regulated environments.

How can fintech companies measure the ROI of generative AI?

Track ROI across three dimensions: efficiency (document processing time, per-function headcount cost), revenue impact (customer retention, product adoption), and risk reduction (fraud losses, compliance penalty avoidance). Set baseline metrics before deployment — that single step makes post-launch measurement straightforward.