Introduction

Generative AI in financial services has crossed a threshold. What started as isolated pilots at the largest global banks is now running in production across institutions of every size — community banks, regional credit unions, and global asset managers alike.

Juniper Research projects bank spending on Gen AI to grow from $6 billion in 2024 to $85 billion by 2030 — over 1,400% growth in six years. That figure alone signals this isn't a trend to monitor from the sidelines.

For financial institutions, the window to build a durable Gen AI advantage is open — but not indefinitely. Organizations that establish these capabilities now are already pulling ahead on efficiency, customer experience, and risk management. The longer others wait, the harder each of those gaps becomes to close.

This article covers what financial services leaders need to know right now:

- Use cases generating real, measurable results today

- Strategic benefits already being realized across institutions

- Emerging trends shaping the next wave of adoption

- Challenges worth preparing for before they become blockers

- The infrastructure foundation that makes it all work

Key Takeaways

- Bank Gen AI spending is projected to grow 1,400% between 2024 and 2030, reaching $85 billion

- McKinsey estimates Gen AI could add $200B–$340B in annual value to banking — 9–15% of operating profits

- Top use cases already delivering ROI: fraud detection, compliance automation, hyper-personalized lending, and document processing

- Only 8% of banks are developing Gen AI systematically; most remain in tactical mode

- Agentic AI and hyper-personalization represent the next major wave of financial services transformation

- Cloud infrastructure determines whether Gen AI deployments scale across the enterprise or plateau at the pilot stage

What Is Generative AI in Financial Services?

Generative AI refers to advanced models — primarily large language models (LLMs) and multimodal systems — that generate new content, insights, predictions, and responses by learning patterns from massive datasets.

The key distinction from traditional banking automation: rule-based systems follow explicit instructions. Gen AI understands context, interprets unstructured information, and produces novel outputs.

That distinction has direct implications for financial services, where most of the valuable data is anything but structured:

- Data is predominantly unstructured — contracts, emails, analyst reports, regulatory filings, call transcripts

- Regulatory complexity demands constant interpretation, not just rule execution

- Customer expectations have shifted toward personalized, real-time engagement

- Operational cost pressure is relentless across lending, compliance, and servicing

McKinsey estimates Gen AI could add $200 billion to $340 billion in annual value to banking, equal to 9–15% of operating profits. That's a fundamental shift in how banks operate, not an incremental upgrade.

Yet adoption remains uneven. IBM's 2024 research found that only 8% of banks were developing Gen AI systematically, while 78% had taken a purely tactical approach. For financial institutions still in tactical mode, that gap is where competitors are quietly pulling ahead.

High-Impact Use Cases Already Transforming Financial Services

Intelligent Customer Engagement and Support

AI-powered assistants have moved well past simple FAQ bots. Today's deployments handle complex account queries, deliver personalized financial guidance, process requests, and route escalations — available continuously without staffing constraints.

The real-world proof points are compelling:

- Morgan Stanley deployed its AI @ Morgan Stanley Assistant, powered by OpenAI, achieving 98% adoption by advisor teams. Its follow-on tool, AI @ Morgan Stanley Debrief, generates meeting notes and CRM entries automatically — saving advisors approximately 30 minutes per client meeting

- HSBC uses Gen AI to support 3 million client interactions annually across its corporate and institutional banking teams, with 88% of clients rating the bank easy to deal with

- Klarna launched an OpenAI-powered assistant that handled 2.3 million conversations in its first month — performing work equivalent to 700 full-time agents

- NatWest upgraded its Cora digital assistant to Cora+, building on a base that handled 10.8 million customer queries in 2023

The pattern across these deployments is consistent: Gen AI handles the repetitive, time-consuming work so human advisors can focus on the conversations that actually build client relationships.

Fraud Detection and Risk Intelligence

Legacy fraud systems flag anomalies based on predefined rules. Gen AI learns normal patterns across billions of transactions and detects deviations in real time — including patterns no human analyst would have thought to encode as a rule.

Mastercard's Decision Intelligence Pro illustrates the gap. According to Mastercard's own data, the system scans 1 trillion data points in under 50 milliseconds, boosts fraud detection by 20% on average (and up to 300% in some cases), and reduces false positives by more than 85%.

Fewer false positives means fewer legitimate transactions blocked — a direct customer experience improvement alongside the security benefit.

Beyond detection, Gen AI generates synthetic fraudulent transaction data to train algorithms against attack vectors that haven't occurred yet. Financial institutions can stress-test their defenses against threats before those threats materialize.

Automated Compliance and Regulatory Reporting

Compliance is consuming an ever-larger share of bank resources. BPI research found that bank employee hours dedicated to compliance increased 61% between 2016 and 2023, with regulatory obligations consuming roughly 42% of C-suite time.

Gen AI addresses this by:

- Summarizing regulatory updates across jurisdictions and mapping them to internal policies

- Drafting audit-ready reports from structured and unstructured source data

- Generating responses to regulator queries with citation-backed documentation

- Automating gap analysis between current policies and new requirements

The result is compliance teams spending less time on document production and more time on interpretation and strategy.

Credit Decisioning and Loan Processing

Traditional underwriting is document-heavy, time-consuming, and inconsistent across analysts. Gen AI changes each of those variables.

Moody's notes that AI-powered credit memos can now be produced in minutes rather than the hours of manual underwriter effort previously required. Gen AI tools review documents, flag policy violations, identify missing information, and synthesize data from multiple sources into structured credit memos. No individual analyst can match that consistency at scale.

For smaller financial institutions competing against large banks for commercial borrowers, faster turnaround isn't just an efficiency win. It's a competitive differentiator.

The Strategic Benefits Financial Institutions Are Realizing

Operational Efficiency at a Different Level

Gen AI automates complex, judgment-intensive workflows — not just repetitive data entry. That scope changes the efficiency math considerably.

Accenture research found that 73% of US bank employee time has high potential to be impacted by Gen AI — 39% through automation and 34% through augmentation. Early adopters could see 22–30% productivity improvements over three years. McKinsey's analysis suggests Gen AI could reduce customer-care costs by 30–45% and cut human-serviced contacts by up to 50%.

Better Decisions, Faster

Gen AI processes structured and unstructured data simultaneously: market trends, credit histories, earnings call transcripts, and real-time signals handled in a single analytical pass. Risk assessments become more comprehensive. Investment research gets faster without sacrificing depth.

Personalization at Scale

Speed and analytical depth matter at the institutional level. At the customer level, the impact looks different. Historically, personalized financial guidance was reserved for high-net-worth clients. Gen AI changes that by enabling:

- Tailored product recommendations based on individual financial behavior

- Personalized communications that adapt to customer context

- 24/7 advisory support that responds to specific financial situations

Personalization shifts from a premium tier to a baseline expectation — and institutions that make that shift early tend to hold customers longer.

New Revenue Streams and Competitive Access

Early Gen AI adopters aren't just cutting costs. They're launching AI-native financial products, entering markets faster, and competing on service capabilities that previously required much larger teams. Smaller institutions now have a credible path to compete with the largest banks on service sophistication — without the headcount to match.

The Future Outlook: Emerging Trends Shaping Gen AI in Finance

The first wave of Gen AI adoption focused on single-task automation — one assistant, one workflow, one department. The second wave is about interconnected, autonomous systems. Financial institutions that aren't preparing now will be reacting to this shift rather than leading it.

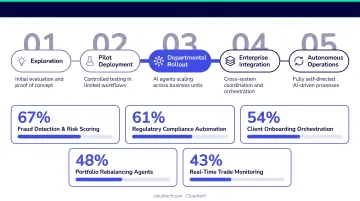

The Rise of Agentic AI in Financial Operations

Agentic AI systems don't just answer questions — they take multi-step actions autonomously to achieve defined goals. A portfolio monitoring agent, for example, doesn't wait to be asked about a risk threshold breach. It detects the breach, generates a report, and alerts the relationship manager — without human prompting at each step.

A Capgemini survey found that 80% of financial services firms are in ideation or pilot stage for AI agents, with top use cases including:

- Customer service (75%)

- Fraud detection (64%)

- Loan processing (61%)

Only 10% have implemented at scale — meaning the competitive window to lead is still open.

Hyper-Personalized Financial Products and Advisory

The next frontier moves beyond personalized communications to individualized product creation. Gen AI will enable financial institutions to generate bespoke loan structures, investment allocations, or insurance terms tailored to a single customer's profile, goals, and behavioral patterns — in real time, at scale.

This shifts product design from segment-based to genuinely individual.

Gen AI-Powered RegTech and Proactive Compliance

The RegTech market is valued at $20.67 billion in 2025, projected to reach $44.11 billion by 2030. Financial services accounts for nearly 58% of that market.

Gen AI's role within RegTech is evolving from reactive to proactive — continuously monitoring regulatory changes across jurisdictions, automatically mapping them to internal policies, and flagging gaps before they become violations. As global regulations around AI itself continue to evolve, this capability becomes a compliance requirement, not just an efficiency gain.

Convergence with Tokenization, Blockchain, and Open Banking

Gen AI is beginning to intersect with tokenization of real-world assets, blockchain-based settlement, and open banking APIs — a convergence that's enabling entirely new financial products. Oliver Wyman has documented how blockchain and Gen AI together are changing how banks structure deals and manage client relationships.

Financial institutions building modular AI architectures today — ones that can connect to new data sources and settlement layers as they emerge — will absorb these shifts as opportunities rather than disruptions.

Key Challenges and How Financial Institutions Can Navigate Them

Data Privacy, Security, and Governance

Financial data is among the most sensitive and regulated in any industry. Gen AI systems that ingest this data must operate within strict controls:

- Data anonymization before model ingestion

- Role-based access management limiting what each system can see

- Model output auditing to catch inappropriate disclosures

- Vendor data handling policies — particularly whether prompts are used for model training

Poorly governed AI creates both regulatory exposure and reputational risk. Governance can't be retrofitted after deployment.

Model Accuracy, Hallucination Risk, and Bias

In financial services, a confident but wrong answer carries real consequences. An AI that generates inaccurate data in a credit memo or regulatory report doesn't just create rework — it creates liability.

Managing this requires:

- Fine-tuning models on domain-specific financial data

- Human oversight checkpoints at high-stakes decision points

- Continuous bias monitoring, particularly in credit scoring and lending

- Retrieval-augmented generation (RAG) architectures that anchor responses in verified source documents

Legacy System Integration and Talent Gaps

Even when the AI strategy is sound, execution runs into structural barriers. The Bank of England and FCA's 2024 AI survey found that 46% of financial firms had only a partial understanding of the AI technologies they use, with data protection and insufficient talent identified as leading constraints.

Two obstacles consistently derail Gen AI programs past the pilot stage:

- Legacy infrastructure incompatibility — many institutions, particularly smaller ones, run core banking systems decades old and not natively built for modern AI frameworks

- AI talent gaps — connecting legacy pipelines to Gen AI without introducing data integrity or security issues requires specialized expertise most institutions don't have in-house

Addressing both requires either building internal capability deliberately or engaging implementation partners who can bridge the technical and organizational gaps from the start.

The Cloud and Infrastructure Foundation That Makes It All Work

Gen AI at scale in financial services is fundamentally an infrastructure problem. Securely storing and processing sensitive financial data, running inference at low latency, maintaining regulatory compliance, and scaling on demand all require a purpose-built cloud architecture.

Core Infrastructure Requirements

Financial services Gen AI deployments need:

- Secure data pipelines — governed ingestion of structured and unstructured financial data

- Vector databases and RAG architecture — enabling AI to retrieve from verified source documents rather than generate from memory alone

- Governed access controls — role-based permissions with full audit logging

- Monitoring frameworks — catching model drift, anomalous outputs, and compliance deviations in real time

- Compliance alignment — SOC 2, PCI-DSS, and other financial services regulatory standards built into the architecture, not added later

AWS provides the foundational services — compute, storage, managed ML services, and security controls — that make this architecture buildable without starting from scratch.

Amazon Bedrock, for example, is listed in scope for SOC 1, SOC 2, SOC 3, and PCI DSS compliance programs, with data encrypted in transit and at rest, and prompts not used to train AWS models or shared with third parties.

Why SMBs and Mid-Market Firms Need the Right Partner

Most smaller financial institutions don't have the internal cloud expertise to architect a Gen AI-ready AWS environment correctly — one that meets financial services compliance requirements from day one.

Cloudtech, an AWS Advanced Tier Partner based in New York, helps financial services firms design and deploy Gen AI-ready AWS architectures with security and compliance guardrails built in from the start. The core toolset includes:

- Intelligent document processing via Amazon Textract

- RAG architectures built on Amazon Bedrock and Amazon OpenSearch

- Natural language interfaces via Amazon Q Business

Every deployment runs within the client's own AWS environment, preserving full data ownership and audit logging.

For institutions looking to move from pilot to production, that combination of pre-built accelerators and compliance-ready architecture typically cuts deployment timelines from months to weeks.

Frequently Asked Questions

What is the use of generative AI in financial services?

Gen AI is used across customer service, fraud detection, compliance reporting, loan processing, and investment research. Its core strength is processing unstructured data — documents, transcripts, regulatory filings — and turning it into relevant, actionable outputs that accelerate decision-making across the institution.

How does generative AI differ from traditional AI in banking?

Traditional AI in banking follows predefined rules or pattern-matching logic: flag this transaction type, approve loans above this score. Gen AI learns from vast datasets and generates new content, narratives, and insights. It can draft reports, explain decisions in plain language, or simulate financial scenarios that no rule was written to handle.

What are the biggest risks of deploying generative AI in financial services?

The three primary risks are: model hallucinations producing inaccurate outputs that inform high-stakes decisions, data privacy and security vulnerabilities when sensitive financial data enters AI systems without proper controls, and regulatory compliance risk as AI governance frameworks continue to evolve globally — including regulations specifically targeting AI systems.

How will generative AI change the role of financial advisors and analysts?

Gen AI will automate research compilation, report generation, and routine analysis, shifting advisors and analysts toward client relationship management, strategic interpretation, and decisions that require contextual judgment. The role changes, but the human layer becomes more valuable, not less.

What infrastructure does a financial institution need to run generative AI?

The core requirements: secure cloud infrastructure with financial-grade compliance controls, robust data pipelines, vector databases for retrieval-augmented generation, model serving and monitoring capabilities, and governance frameworks. AWS provides the foundational services and security architecture — including Amazon Bedrock, which is in scope for SOC and PCI DSS compliance programs.

How long does it take to implement generative AI in a financial services firm?

Timelines depend on use case complexity and infrastructure maturity. Focused deployments, like a compliance summarization tool or an AI customer service assistant, can reach production in weeks on pre-configured cloud foundations. Multi-system integrations take longer but follow the same phased approach.