Introduction

Loan servicing operations are under compounding pressure. The MBA reports fully loaded servicing costs of $176 per performing loan and $1,573 per nonperforming loan in 2024 — figures that make every unanswered call and manual inquiry resolution an expensive problem.

At the same time, borrower expectations have shifted. J.D. Power's 2025 mortgage servicer digital experience study found only 44% of servicer apps provide basic functionality and just 12% deliver genuinely valuable digital experiences. Borrowers want answers at midnight, not hold times above ten minutes.

Conversational AI addresses both sides of that gap — deflecting routine inbound volume, automating payment workflows, and enabling 24/7 borrower self-service across voice, chat, SMS, and email without proportionally scaling headcount.

Adoption is accelerating: a 2024 Gartner survey of 187 customer service leaders found 85% planned to explore or pilot conversational GenAI in 2025. Servicers that haven't evaluated their options are already behind.

This guide cuts through the noise — evaluating the top conversational AI platforms for loan servicing in 2026 across capabilities, compliance readiness, and fit for your operation's specific needs.

Key Takeaways

- Conversational AI automates borrower interactions across voice, chat, SMS, and email — handling payments, inquiries, and account updates without manual intervention

- Choosing the wrong platform means slow LMS integrations, compliance gaps, and months-long deployments — the right fit matters

- AWS-native solutions (Amazon Connect + Lex) offer distinct advantages for lenders already on AWS infrastructure

- Compliance requirements — FDCPA, TCPA, UDAAP — must be native to the platform, not bolted on afterward

- A well-matched platform lowers cost per loan serviced, reduces inbound call volume, and lifts borrower satisfaction — often within the first quarter of deployment

What Is Conversational AI in Loan Servicing?

Traditional IVR routes calls through rigid menu trees. Conversational AI goes further: it understands natural language, maintains context across a multi-turn exchange, and executes transactions rather than simply directing callers to a queue.

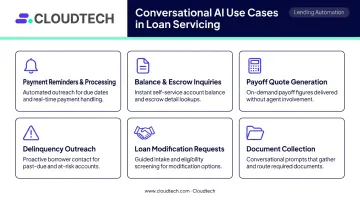

In the loan servicing context, that means NLP- and ML-driven systems that connect directly to your loan management system (LMS) and handle requests end-to-end, including:

- Payment reminders and processing — automated outreach and self-service payment capture

- Balance and escrow inquiries — real-time account data delivered without agent involvement

- Payoff quote generation — calculated on live loan data and delivered via the borrower's preferred channel

- Delinquency outreach — proactive, compliant contact at scale

- Loan modification and loss mitigation requests — intake and routing with full context transfer

- Document collection — automated requests with status tracking

The critical differentiator between a conversational assistant and a full servicing agent is LMS write-back. Platforms that can only read account data still require human agents to complete transactions. Platforms with write-back capability close the loop automatically: updating payment status, logging interactions, and triggering downstream workflows in real time.

The 2026 market spans AWS-native infrastructure tools, purpose-built vertical SaaS, and enterprise contact center platforms — each with distinct trade-offs in integration depth, compliance posture, and total cost of ownership.

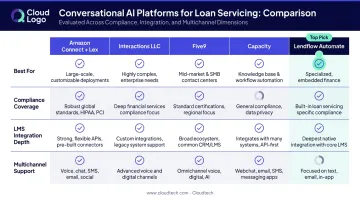

Best Conversational AI Platforms for Loan Servicing in 2026

These platforms were evaluated across five dimensions: financial services compliance readiness, LMS/LOS integration depth, multichannel coverage, scalability, and proven deployment in regulated lending environments. The right fit depends on your servicing volume, existing infrastructure, and how much customization control your team needs.

Amazon Connect + Amazon Lex

Amazon Connect is AWS's cloud contact center platform. Amazon Lex is its NLP engine for conversational AI. Together, they form a fully managed, AWS-native stack that loan servicers can deploy within existing cloud infrastructure — no third-party vendor required.

The architecture is designed for full servicer control: Amazon Connect invokes Lex for intent recognition, AWS Lambda handles workflow logic and API calls, and Amazon Bedrock handles generative AI responses when Lex encounters unrecognized intents. Every compliance configuration, data residency rule, and integration pattern stays in-house — not delegated to a vendor.

NatWest deployed this combination to classify more than 1,600 voice intents across production, demonstrating the scale this architecture supports in a regulated financial services environment. Standard Bank reported 42% fewer missed calls after Amazon Connect adoption.

| Feature Area | Details |

|---|---|

| Key Features | Omnichannel voice + chat, NLP-powered self-service, real-time call transcription, contact flow builder, AWS Lambda-based workflow triggers, Amazon Bedrock generative AI integration |

| Best For | Loan servicers already on AWS who need a fully customizable, compliance-configurable conversational AI stack without vendor lock-in |

| Compliance & Integration | HIPAA-eligible, PCI DSS in scope, SOC-covered; requires configuration for FDCPA/TCPA workflows — best deployed with an AWS-certified implementation partner |

Interactions LLC

Where most conversational AI platforms rely entirely on automation, Interactions LLC (now part of SoundHound AI) takes a different approach. Its Intelligent Virtual Assistant serves financial services clients through a hybrid model that pairs AI with human oversight — a distinction that matters in loan servicing.

When the AI encounters ambiguous input — a nuanced payment dispute, an unusual loss mitigation scenario — human Intent Analysts intervene to resolve the intent, then return control to the automated system. This matters in loan servicing, where borrower queries routinely fall outside clean intent patterns. The result is higher task completion rates than purely automated systems can deliver.

| Feature Area | Details |

|---|---|

| Key Features | Hybrid AI + human-assisted NLU, high-accuracy intent resolution, payment and account action processing, quality assurance monitoring, complex borrower interaction handling |

| Best For | Large servicers with complex borrower interaction profiles — particularly those prioritizing completion accuracy and compliance auditability over automation throughput |

| Compliance & Integration | Compatible with major CXaaS, UCaaS, and CRM platforms; built-in QA monitoring for regulated disclosures |

Five9

Five9 is a cloud contact center platform with an expanding AI layer built for financial services. Its differentiator is breadth: loan servicers can run AI voice bots for self-service while equipping live agents with real-time transcription, suggested responses, and compliance monitoring — all within the same environment.

Five9's resource catalog references RoundPoint Mortgage receiving over 570,000 calls monthly on its platform, providing production-scale evidence in the mortgage servicing space specifically. Five9 also documents the ability to analyze up to 100% of interactions through its quality management tooling — relevant for UDAAP audit requirements.

| Feature Area | Details |

|---|---|

| Key Features | AI voice bots, real-time agent assist, intelligent routing, omnichannel voice and digital engagement, workflow automation, real-time transcription and compliance monitoring |

| Best For | Mid-to-large servicers seeking an infrastructure-first contact center AI that scales under peak call volumes while supporting both self-service and agent-assisted interactions |

| Compliance & Integration | Pre-built adapters for Salesforce, ServiceNow, Microsoft Dynamics, Zendesk, and Oracle; REST APIs for custom LOS/MSP connectivity |

Capacity

Capacity is an AI-powered support automation platform with documented financial services deployments. Its standout feature for loan servicing operations teams is a no-code knowledge management layer — servicing staff can configure and update borrower-facing responses without engineering involvement.

That matters when compliance-sensitive disclosures change or loan program terms are updated. Rather than filing a ticket and waiting for a developer, compliance and operations teams update the knowledge layer directly. Capacity also manages routing, escalation, and cross-channel continuity without heavy IT dependency, with 250+ pre-built integrations including Salesforce and major helpdesk platforms.

| Feature Area | Details |

|---|---|

| Key Features | AI voice and chat automation, no-code knowledge base configuration, multichannel support, real-time escalation routing, continuous learning from servicing workflows |

| Best For | Servicers seeking rapid borrower self-service deployment across channels without dedicated engineering resources for ongoing maintenance |

| Compliance & Integration | 250+ pre-built integrations including Salesforce and HubSpot; API connectivity for custom servicing platforms |

Lendflow Automate

Every other platform on this list started as a general-purpose contact center tool adapted for lending. Lendflow Automate is the exception — built specifically for the commercial lending lifecycle, with agents configured for SMB lending from the ground up: Voice AI, AI Chatbot, Doc Analyzer, Trust Score, and AI Email Inbox in a single orchestrated platform.

The platform supports diverse commercial products: term loans, MCAs, lines of credit, and factoring — each with variable documentation requirements that general tools handle poorly. It's SOC 2 Type II certified and connects to 75+ lenders via a single endpoint, making it particularly suited to embedded lending platforms and fintech lenders managing multi-product portfolios.

| Feature Area | Details |

|---|---|

| Key Features | Specialized agents for voice, chat, email, document analysis, and trust scoring; real-time portfolio monitoring; automated payment reminders and retry logic; borrower self-service portals; dynamic delinquency prioritization |

| Best For | SMB lenders and fintech platforms managing diverse commercial loan products who need AI that handles full-lifecycle servicing — not just inbound call deflection |

| Compliance & Integration | SOC 2 Type II certified; integrates with 75+ lenders via single endpoint; API-first architecture for CRM and LMS connectivity |

Key Features to Look for in a Conversational AI Platform

Multichannel Coverage

Borrowers don't stay in one channel. They call, then follow up by text, then check a portal. Platforms that cover only voice create gaps that require separate tooling and fragment the borrower record.

Look for native continuity across:

- Voice (inbound and outbound)

- SMS and text messaging

- Web chat and mobile app chat

Context should carry across all of them. A borrower who started a payment conversation by phone shouldn't have to repeat their account number when they follow up via SMS.

LMS Integration Depth

This is where most buyer evaluations fall short. The difference matters:

- Read-only access — the platform displays account data, but a human agent must complete any transaction

- Full write-back capability — the platform updates payment status, logs interactions, triggers modifications, and closes the loop without human involvement

Always ask vendors to demonstrate write-back capability against your specific LMS or MSP before committing. Servbank's case-reported 80% call deflection and 30% cost reduction shows what deep integration can produce. Those numbers only hold when the platform completes transactions — not just displays data.

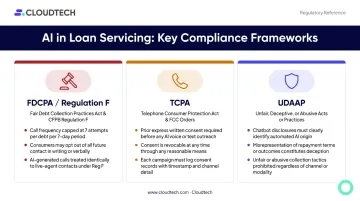

Compliance Framework Requirements

Loan servicing sits at the intersection of multiple federal regulations. Any platform you evaluate must handle these natively:

- FDCPA / Regulation F — call frequency limits (presumptive compliance at no more than 7 calls in 7 consecutive days per debt), required debt-collection disclosures, and electronic opt-out for text and email communications

- TCPA — the FCC has confirmed that AI-generated voices fall under TCPA's artificial/prerecorded-voice rules, requiring prior express consent for calls and texts; consumers may revoke consent through any reasonable method

- UDAAP — the CFPB has warned that chatbots providing inaccurate information or blocking access to human assistance can constitute unfair, deceptive, or abusive acts

Audit trails, opt-out management, call recording, and escalation to human agents are not optional add-ons. Ask every vendor for documented evidence of how each is handled — gaps here create regulatory exposure that no servicing operation can afford.

How We Chose the Best Conversational AI for Loan Servicing

The most common buyer mistake: selecting platforms based on voice quality or demo experience rather than integration depth, compliance governance, and escalation logic. Those three factors determine real-world performance in a regulated servicing environment.

Evaluation criteria used:

- Native LMS/MSP integration and write-back capability — can the platform complete transactions, not just retrieve data?

- Built-in compliance governance — are FDCPA, TCPA, and UDAAP requirements handled natively, with audit trail documentation?

- Escalation handling quality — does full loan context transfer to human agents when escalation occurs?

- Use case depth — does the platform cover payments, modifications, and loss mitigation, or only FAQ deflection?

- Deployment speed and total cost of ownership — how long to production, and what are the ongoing costs at scale?

For loan servicers operating on AWS, Amazon Connect and Lex carry a meaningful advantage in data residency control, security configuration, and cost management. How well that advantage translates depends heavily on the underlying infrastructure decisions — which is why the platforms below are evaluated against all five criteria, not just feature lists.

Conclusion

The best conversational AI for loan servicing in 2026 is the platform that integrates directly with your servicing systems, handles compliance requirements without custom development, and scales to peak borrower volumes without degrading the experience.

Before committing to any platform, request three things during any pilot engagement:

- Proof of LMS write-back capability against your specific system

- Audit trail documentation covering FDCPA, TCPA, and UDAAP requirements

- Stress-test results at your anticipated peak call volumes

For financial services companies deploying conversational AI on AWS, the underlying infrastructure matters as much as the platform itself. Cloudtech's AWS-certified architects design and implement the cloud foundation, Generative AI on Bedrock integrations, and compliance-ready AWS environments these solutions require to run reliably at scale. Contact Cloudtech to discuss your loan servicing AI infrastructure roadmap.

Frequently Asked Questions

What is conversational AI in loan servicing?

Conversational AI in loan servicing refers to NLP- and ML-powered systems that handle borrower interactions across voice, chat, SMS, and email — automating tasks like payment processing, balance inquiries, and account modifications without human agents. These systems integrate directly with loan management systems for real-time data access and transaction execution.

How does conversational AI reduce loan servicing costs?

AI deflects high-volume routine inquiries from human agents, enables 24/7 service without staffing increases, and reduces cost per interaction significantly. With MBA reporting $176 per performing loan in fully loaded servicing costs, even modest deflection rates produce substantial savings at portfolio scale.

What compliance regulations must conversational AI for loan servicing support?

Platforms must support FDCPA, TCPA, and UDAAP — covering debt collection rules, AI call/text consent requirements, and prohibitions on deceptive borrower communications. Audit trails, opt-out management, call recording, and human escalation paths must be built in, not bolted on.

Can conversational AI integrate with existing loan management systems?

Leading platforms offer pre-built connectors or API integrations for major LMS and MSP platforms. The key question to verify: does the platform support read-only data access or full write-back capability? Only write-back allows the AI to complete transactions without human involvement.

What is the difference between conversational AI and traditional IVR for loan servicing?

Traditional IVR routes calls through rigid menu trees with no contextual understanding. Conversational AI understands natural language, handles unexpected queries, and maintains context across a full conversation. The result: higher task completion rates and better borrower satisfaction scores.

How long does it take to deploy a conversational AI solution for loan servicing?

Timelines vary by platform and integration complexity. No-code platforms like Capacity can go live in days to weeks. Deeply integrated AWS-native solutions like Amazon Connect + Lex typically require 30–90 days for proper compliance configuration and LMS integration — though working with an AWS-certified implementation partner can compress that timeline significantly.