Introduction

Bank of America's virtual assistant Erica has surpassed 3 billion client interactions and averages over 58 million conversations per month. That's a single institution's bot. Scale that across the industry, and it's clear that banking chatbots have moved well past experiment status.

The promise is real: automated self-service cuts costs, extends availability to 24/7, and meets the instant-response expectations of younger account holders. The risk is equally real.

The CFPB has documented how poorly built chatbots trap customers in "doom loops," fail to recognize disputes, and expose banks to consumer protection liability. A chatbot that frustrates customers or violates Regulation E is a compliance problem, not just a customer service one.

This guide covers what bank chatbots actually are in 2026, where they create the most value, how to implement them on modern cloud infrastructure, and the security and compliance considerations that no financial institution can afford to skip.

Key Takeaways

- Banking chatbots have evolved from simple FAQ bots to agentic AI systems that execute multi-step workflows

- High-impact use cases span customer support, onboarding, fraud alerts, personalized guidance, and employee productivity

- Successful deployment requires core banking system integration, cloud infrastructure, and compliance built in from day one

- Skipping human escalation paths creates "doom loops" — a documented regulatory risk under CFPB oversight

- Banks that deploy chatbots with proper integrations report containment rates above 80%, cutting live-agent volume significantly

What Are Bank Chatbots and How Have They Evolved in 2026?

Bank chatbots are conversational AI interfaces that use natural language processing (NLP) and large language models (LLMs) to understand customer intent and execute banking tasks: balance inquiries, fund transfers, dispute flagging, and more, across web, mobile, and messaging channels.

Not all chatbots work the same way. Rule-based systems follow fixed decision trees — they answer "What's my balance?" but fail the moment phrasing shifts. LLM-powered systems handle intent, ambiguity, and multi-turn context. Agentic systems go further: they autonomously execute multi-step workflows, not just retrieve information.

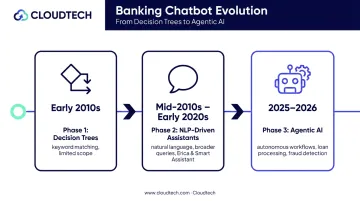

The Evolution in Three Phases

Phase 1 — Decision trees (early 2010s): Keyword matching, limited scope, high frustration rates when customers deviated from expected phrasing.

Phase 2 — NLP-driven assistants (mid-2010s to early 2020s): Bank of America launched Erica in 2018; U.S. Bank followed with its Smart Assistant in 2020. These systems understood natural language and handled a broader range of queries. Erica's scale, nearly 50 million users and over 3 billion cumulative interactions, defined what was possible in this era.

Phase 3 — Agentic AI (2025–2026): McKinsey describes agentic AI as systems that interpret objectives, break them into subtasks, and act with minimal human input. Chatbots in this phase process loan applications, detect fraud patterns, and deliver personalized financial guidance — capabilities that go well beyond simple account lookups.

Where the Industry Stands

Those three phases describe the technology arc, but adoption tells a different story. A 2024 SAS survey of 243 senior banking executives found 60% of banks used generative AI to some degree, yet only 17% had fully integrated it into regular processes. Most institutions are still running pilots. Banks that have moved from experimentation to full deployment share one trait: a deliberate, structured implementation approach rather than ad hoc rollouts.

Top Use Cases for Bank Chatbots in 2026

Customer-Facing Use Cases

24/7 customer support and self-service

High-volume, low-complexity requests are the natural starting point: account balance checks, transaction history, password resets, bill pay, and fund transfers. Handling these interactions automatically frees human agents for complex cases that require judgment.

NatWest's generative AI upgrade to its Cora assistant offers a concrete example of what containment can look like. Their Cora+ proof of concept produced a 67% reduction in customers needing a human adviser and a 150% improvement in customer satisfaction for the tested journeys — though these are proof-of-concept results from a single bank, not industry benchmarks.

Customer onboarding and KYC

Onboarding is the highest-friction touchpoint in retail banking. Chatbots that guide new customers step by step through account opening, collect KYC documentation, and explain terms in plain language directly reduce abandonment rates. Speed and clarity at this stage translate into conversion — a chatbot that stumbles during onboarding hands the customer back to a competitor.

Personalized financial guidance and proactive engagement

The shift from reactive FAQ bot to proactive financial assistant is where the real competitive differentiation appears. Modern chatbots analyze spending patterns, flag unusual transactions, recommend better savings rates, and surface relevant product offers based on actual financial history.

Accenture's 2025 global banking consumer study found 72% of customers said personalization influenced their bank choice, while 62% were open to an AI-powered financial assistant for real-time coaching. Those numbers signal clear demand.

The same study found 84% worried about how banks use their data. That gap means transparency and consent aren't optional features — they're prerequisites for any personalization rollout.

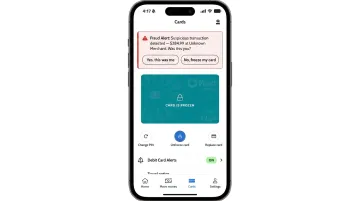

Fraud detection and payment alerts

Capital One's Eno flags suspicious and duplicate charges, alerts customers to unusual recurring transactions, and guides them toward resolution or card locking — all without requiring a call to a support line. The functionality is well-documented; specific fraud-outcome metrics from Eno remain undisclosed.

Chatbots integrated with fraud detection systems give customers immediate control over their accounts. A customer who can freeze a card in 15 seconds through a chat interface is better protected than one waiting on hold.

Employee-Facing Use Cases

Internal productivity tools

Agent assist tools represent an underused application. Internal chatbots handle tasks that quietly drain agent time throughout the workday:

- Surface relevant customer context during live calls

- Retrieve policy documentation without navigating multiple dashboards

- Automate post-call summaries, reducing wrap-up time

- Give relationship managers and compliance teams instant access to regulatory guidelines

The result is faster service and fewer errors — without adding headcount.

How Bank Chatbots Improve Customer Experience: Key Benefits

Operational efficiency and cost reduction

The key metric here is containment rate — the percentage of issues the chatbot resolves without human intervention. Higher containment means lower cost-to-serve. It also means elastic operations: the ability to handle 10x the interaction volume during peak periods without proportionally scaling headcount.

The often-cited $0.50–$0.70 savings per chatbot interaction comes from a 2017 Juniper Research forecast — useful for directional thinking but not a current benchmark. What is verifiable is the NatWest Cora+ proof-of-concept result showing a 67% reduction in human adviser handoffs, which illustrates the cost deflection potential when a well-trained system handles the right interactions.

Faster resolution and higher customer satisfaction

J.D. Power's 2026 U.S. Digital Banking and Credit Card Mobile App Satisfaction Study found virtual assistant users scored satisfaction at 736 out of 1,000 — 18 points higher than non-users. The same study, however, documented sharp satisfaction declines for complex tasks: fraud resolution, charge disputes, and poor human escalation paths all performed significantly worse.

Chatbots reliably improve satisfaction for routine interactions — and just as reliably damage it when pushed into territory they can't handle well. Knowing where to draw that line is the real implementation challenge.

Omnichannel consistency

Modern banking chatbots maintain conversation context as customers move between mobile apps, websites, and voice channels. The contrast with legacy systems is stark: customers previously had to re-authenticate and re-explain their issue on every channel switch.

Eliminating that friction — ensuring a customer who started on mobile doesn't have to repeat themselves when they call in — is a meaningful loyalty driver.

Personalized Guidance for Every Customer

AI chatbots use transaction data and behavioral history to deliver experiences that were previously only possible through dedicated relationship managers. For everyday customers, this means:

- Spending insights surfaced automatically based on actual behavior

- Product recommendations timed to relevant life events or account activity

- Proactive alerts before fees, overdrafts, or missed payments occur

- Financial literacy support delivered at the moment a question arises

Accenture's data showing 88% of Gen Z and Millennials wanting to expand their financial knowledge points directly at this use case. A well-designed chatbot meets both the preference for digital interaction and the demand for practical financial guidance — at the same time.

How to Implement a Banking Chatbot: A Step-by-Step Guide

Step 1 — Define Scope and Priority Use Cases

Start narrow. Banks that try to build a chatbot handling every possible interaction at launch typically produce bloated MVPs that never reach production, or that reach production and perform poorly across the board.

Identify two or three high-volume, high-friction interactions for the initial deployment:

- Account balance inquiries

- Password resets and authentication support

- Payment processing and bill pay status

Define success metrics before building: target containment rate, escalation rate, and CSAT for each use case. Without pre-defined benchmarks, there's no clear signal for when the system is ready to launch — or when it's underperforming post-launch.

Step 2 — Choose the Right Cloud Infrastructure and Integration Architecture

This is the decision that determines whether the chatbot executes real work or just answers static questions. A chatbot disconnected from core banking systems can only surface static information — it cannot transact, retrieve live data, or trigger downstream processes.

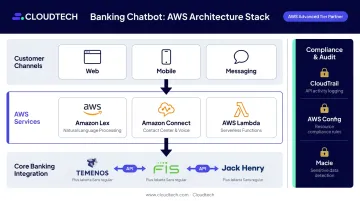

AWS provides a proven, scalable backbone for financial services chatbot deployments:

- Amazon Lex for natural language understanding

- Amazon Connect for cloud contact center integration

- AWS Lambda for serverless execution of banking workflows

The chatbot must connect to core banking systems (Temenos, FIS, Jack Henry, or equivalent) via APIs to perform transactions, retrieve live account data, and trigger downstream processes.

Compliance cannot be an afterthought. Retrofitting it into a live system is expensive and rarely complete.

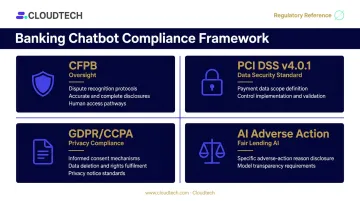

Minimum compliance requirements for a banking chatbot:

- PCI DSS v4.0.1 — mandatory if the chatbot touches cardholder data or any system that could affect the cardholder data environment

- GDPR and CCPA — data privacy obligations apply to all customer data collected during chatbot interactions

- Data residency controls — AWS Region restrictions and sovereignty controls for applicable regulatory requirements

- Audit trail configurations — every interaction that touches sensitive data must be logged and retrievable

AWS-native tools form the compliance instrumentation layer: CloudTrail for audit logging, AWS Config for compliance rule enforcement, and Macie for sensitive data detection. Configure these before the chatbot goes live.

Step 4 — Design Conversation Flows with Clear Escalation Paths

Human escalation paths are non-negotiable. The CFPB has explicitly documented how chatbots that trap customers in repetitive interactions without a path to a human agent create consumer protection violations, not just poor experiences.

Design principles for graceful handoffs:

- Detect frustration signals: repeated questions, explicit requests for a human, negative sentiment

- Transfer full conversation context to the human agent — the customer should never have to repeat themselves

- Offer human escalation proactively after a defined number of failed resolution attempts

- Never block access to human support for disputes or fraud claims

The "doom loop" failure mode — where a customer asks the same question repeatedly and the bot cycles through the same unhelpful responses — is entirely predictable and preventable at the design stage.

Step 5 — Launch, Monitor, and Continuously Improve

Treat a banking chatbot as a live product with ongoing maintenance requirements. Models degrade on stale training data, and conversation flows that worked at launch will break as customer language evolves and new products are introduced.

Post-launch KPIs to instrument from day one:

- Containment rate — percentage of interactions fully resolved without human escalation

- Resolution accuracy — how often the chatbot's answer matches the correct outcome

- Escalation rate — frequency and reasons for human handoffs

- CSAT scores — per interaction, not aggregated, to surface specific failure patterns

- Fallback rate — how often the bot fails to match customer intent

Build a continuous retraining loop using real conversation data. Monthly review cycles — not quarterly — keep the model current and catch degradation before customers notice it.

Security, Compliance, and Common Pitfalls to Avoid

Security Risks Specific to Banking Chatbots

Three threat vectors demand explicit attention:

- Prompt injection attacks: OWASP ranks prompt injection as LLM01:2025 — the top risk for LLM-based systems. Malicious inputs designed to alter chatbot behavior can disclose sensitive information or trigger unauthorized actions

- Phishing impersonation: Attackers deploy fake chatbot interfaces mimicking legitimate bank bots to harvest credentials and account data

- Insecure chat logs: Logs containing PII must be encrypted, access-controlled, and retained only as long as compliance requires

Security requirements beyond what the LLM provider covers:

- Multi-factor authentication before any account action

- End-to-end encryption for all chat sessions

- Real-time fraud detection integration

- Red-team testing before launch and on a recurring schedule

Regulatory Compliance Obligations

The CFPB is explicit: banks remain responsible for consumer financial law compliance when using chatbots. A chatbot that fails to recognize a dispute notice, provides inaccurate fee information, or blocks access to human support can create violations under the Electronic Fund Transfer Act, Regulation E, and fair lending regulations.

The bank — not the technology vendor — bears the legal liability. That liability spans several regulatory areas:

- CFPB oversight — dispute recognition, accurate disclosures, human access requirements

- PCI DSS v4.0.1 — payment data scope determination and control implementation

- GDPR/CCPA — data collection consent, deletion rights, and privacy notices

- AI adverse action requirements — lenders using AI for credit decisions must provide specific, accurate adverse-action reasons; model opacity is not a defense

Common Deployment Mistakes

These failures appear repeatedly in post-mortems and CFPB complaint data:

- Launching without defined use cases — producing a system that handles everything poorly

- Using generic off-the-shelf scripts without banking-specific training data

- Failing to integrate with core systems — creating a static FAQ page with a conversational interface

- Skipping testing with real customer language — slang, abbreviations, and limited English proficiency break rigid NLP models

- No escalation design — the doom loop isn't a bug that appears post-launch; it's a design omission

Each of these failures has a known fix. Addressing them during design costs a fraction of what a post-launch CFPB complaint or customer attrition event will.

Frequently Asked Questions

What is an example of a chatbot in banking?

Bank of America's Erica is the most cited example: over 3 billion interactions and nearly 50 million users since its 2018 launch, covering balance inquiries, spending insights, and proactive alerts. Capital One's Eno handles similar work for cardholders, focusing on fraud detection and charge disputes.

What is the cost of an AI chatbot in 2026?

Costs depend on build approach (custom vs. SaaS vs. cloud-native), integration depth, and compliance requirements. A cloud-native proof of concept on AWS Bedrock can be scoped as a fixed-fee engagement in weeks; complex enterprise deployments with deep legacy integration run considerably higher.

Can bank chatbots replace human customer service agents?

No — but the best implementations don't try. Chatbots handle high-volume routine interactions effectively, but complex disputes, emotionally sensitive situations, and high-value advisory conversations require human judgment. The strongest deployments use chatbots to handle tier-one volume so human agents can focus on the interactions where they add the most value.

How do banking chatbots keep customer data secure?

Security requires multi-factor authentication before account access, end-to-end encryption across all sessions, audit trail logging for every interaction touching sensitive data, and PCI DSS v4.0.1 compliance for any payment data in scope. These controls must be architected in from the start; retrofitting them after launch is both harder and less reliable.

What compliance regulations apply to banking chatbots in the US?

Federal consumer financial law applies in full , including CFPB oversight, Regulation E dispute recognition requirements, and fair lending rules. PCI DSS v4.0.1 covers payment data. GDPR and CCPA govern data privacy depending on customer geography. The financial institution, not the chatbot vendor, is legally responsible for compliance failures.

How long does it take to implement a banking chatbot?

A narrowly scoped, cloud-native deployment (for example, Amazon Lex and Amazon Connect covering two or three defined use cases) can reach a working POC in 4 to 8 weeks. Complex enterprise deployments with deep legacy system integration run 12 months or more. Defining a narrow initial scope is the single largest lever for accelerating time-to-value.