Introduction

Financial institutions are deploying conversational AI faster than their compliance frameworks can keep up. According to the CFPB, roughly 98 million Americans interacted with a bank chatbot in 2022 — a number projected to reach 110.9 million by 2026. Every major U.S. commercial bank has deployed one.

The compliance stakes are real. A single AI-generated response that misrepresents dispute rights, fee structures, or loan terms can constitute a UDAAP violation under federal consumer financial law.

The CFPB has made this explicit: deficient chatbots can provide inaccurate information, fail to recognize federal rights, and impede access to human support. The bank remains fully liable for each of those failures.

"Best" in fintech conversational AI doesn't mean fastest to deploy or highest deflection rate. It means compliance-ready by design: audit trails, hallucination controls, and escalation logic built in before the first customer interaction.

This guide breaks down the top platforms, what separates them technically, and how to evaluate them against the criteria regulators actually care about.

Key Takeaways

- SOC 2 Type II, GDPR, and ISO 27001 are baseline requirements — not differentiators

- Fintech AI queries fall into three risk bands; tools that can't classify risk create direct regulatory liability

- Three capabilities separate compliant tools from risky ones: audit trail depth, hallucination controls, and deterministic escalation logic

- Top platforms covered: Kasisto, Twig, Fini, Kore.ai, and Ada — each evaluated on compliance-critical architecture, not just feature lists

- Cloud infrastructure — data residency, encryption, access controls — is as consequential as the AI tool itself

What Is Conversational AI in Fintech Compliance?

Conversational AI in fintech refers to NLP-driven chat and voice systems that handle customer interactions around account management, KYC verification, AML flag responses, dispute processing, and loan inquiries. This is fundamentally different from general-purpose chatbots.

When an AI system touches regulated financial processes, every response carries potential legal weight.

The Three Risk Bands

Compliant fintech AI platforms classify every inbound query into one of three risk categories:

- Low-risk informational — branch hours, product descriptions, general rates. AI can resolve autonomously.

- Account-specific non-regulated — balance inquiries, transaction history, basic account changes. AI can handle with authentication, but full logging required.

- Compliance-sensitive regulated — disputes, fraud claims, KYC/AML flags, loan decisions, fee waivers. Must escalate to human agents with full conversation context.

Tools that cannot classify query risk automatically create direct regulatory liability. If an AI autonomously resolves a dispute query it should have escalated, the institution owns that outcome. That liability isn't abstract — it's defined by a layered set of regulations that apply whether your institution is ready for them or not.

The Regulatory Landscape

Several frameworks govern fintech conversational AI:

- CFPB consumer protection rules — apply to any AI system providing information about consumer financial products

- OCC third-party risk management (Bulletin 2023-17) — treats conversational AI vendors as third-party relationships requiring due diligence and ongoing monitoring

- NYDFS Part 500 — applies cybersecurity and access control requirements to any AI system processing nonpublic information for licensed New York financial institutions

- GDPR Article 22 gives EU customers the right not to be subject to solely automated decisions with legal or significant effects, requiring human review safeguards for credit and account decisions

- EU AI Act — classifies creditworthiness evaluation and insurance risk pricing AI as high-risk under Annex III, with full compliance obligations applying from August 2, 2026

On penalties: EU AI Act Article 99 sets fines for high-risk AI violations at up to €15 million or 3% of global annual turnover (whichever is higher), with prohibited practice violations reaching €35 million or 7%.

Best Conversational AI for Fintech Compliance

These platforms were evaluated across five criteria — not feature breadth alone:

- Compliance certification depth — what's actually certified, not just claimed

- Hallucination control architecture — how the system prevents incorrect answers by design

- Audit trail capability — whether logs are defensible under regulatory review

- Human escalation design — when and how the AI defers to a human

- Integration maturity — how well it connects to existing banking infrastructure

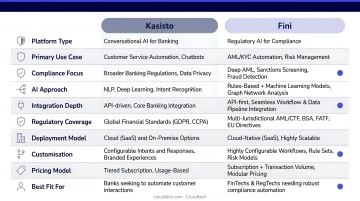

Kasisto (KAI)

Kasisto is the longest-standing banking-specific conversational AI platform, deployed by institutions including Standard Chartered, J.P. Morgan, and DBS Bank. Its KAI platform ships with banking-domain NLU and compliance scaffolding pre-built — not bolted on after the fact.

What sets it apart from general-purpose tools is vocabulary precision. Banking-specific intent classification reduces misclassification rates on queries like "dispute this charge" or "my card was compromised" — exactly the query types where misclassification creates regulatory exposure. Its KAIops layer provides auditability and governed remediation workflows.

Implementation timelines run longer than lighter-weight platforms. Institutions that can support a structured deployment will get the most out of it; those without dedicated resourcing should factor that in early.

| Category | Details |

|---|---|

| Compliance Certifications | SOC 2 Type II |

| Key Features | Banking-domain NLU, pre-built compliance scaffolding, KAIops auditability layer, multi-channel deployment |

| Best For | Retail and commercial banks requiring banking-specialized AI with institutional track record |

Twig

Twig is an autonomous AI support platform built for regulated SaaS and fintech environments. Its distinguishing architecture: every AI response is logged with classified intent, retrieved source, confidence score, and timestamp — creating an audit trail defensible under regulatory review.

Its Human Review module routes low-confidence AI responses through a human reviewer before they reach the customer, rather than sending borderline answers directly. Combined with confidence-based escalation routing, Twig handles autonomous resolution where appropriate and defers where it shouldn't.

For mid-market fintech (Series A through C) that needs high automation rates without sacrificing audit defensibility, Twig is the most operationally practical option in this category.

| Category | Details |

|---|---|

| Compliance Certifications | SOC 2 Type II, GDPR-ready |

| Key Features | Full conversation audit logs, confidence-based routing, Human Review module, PII screening |

| Best For | Mid-market fintech needing autonomous resolution paired with regulator-ready audit trails |

Fini

Fini's architecture takes a different approach to the hallucination problem. Rather than retrieving from documents and guessing at relevance (standard RAG), Fini reasons through support scenarios using approved internal knowledge only — producing an audit-ready explanation for every decision that traces back to verified sources.

This eliminates hallucination risk by design rather than by guardrail — a structural difference, not a settings toggle. Clients including ICICI Bank use Fini for sensitive workflows: KYC checks, account changes, and refund processing, all with full decision traceability.

In environments where an incorrect AI answer creates UDAAP exposure, that traceability is a direct risk reduction. Reasoning-first architecture isn't just a technical preference — it changes what you can defend in an exam.

| Category | Details |

|---|---|

| Compliance Certifications | SOC 2 Type II, GDPR, ISO/IEC 27001 |

| Key Features | RAGless reasoning architecture, audit-ready decision traces, sensitive workflow automation |

| Best For | Regulated fintech where accuracy and decision traceability are non-negotiable |

Kore.ai

Kore.ai is the enterprise-grade option for financial institutions with complex multi-channel and multi-region operations. It handles voice and chat across 30+ channels, supports NLP in 100+ languages, and includes pre-built templates for core banking processes — account opening, loan applications, payment workflows.

Its depth of integration with core banking systems and enterprise security certifications (SOC 2 Type II, ISO 27001, PCI DSS, GDPR, CCPA) make it the strongest fit for large institutions. Implementation is vendor-managed and suited to organizations with dedicated technical resources to support a full enterprise deployment.

| Category | Details |

|---|---|

| Compliance Certifications | SOC 2 Type II, ISO/IEC 27001, PCI DSS, GDPR, CCPA |

| Key Features | Voice + chat on 30+ channels, pre-built banking and insurance templates, 100+ language NLP |

| Best For | Large banks and financial institutions with complex multi-channel and multi-region requirements |

Ada

Ada's differentiator is non-technical control. Its conversation builder lets compliance and operations teams build, review, and approve every customer-facing response path without engineering involvement. For financial institutions with strict content governance requirements, that removes a major bottleneck — compliance doesn't wait on an engineering sprint to update a regulated response.

Compliance teams can lock down regulated response flows, require approval before any change goes live, and trigger proactive messaging based on customer behavior.

Ada's security certifications cover SOC 2 Type II, GDPR, HIPAA, and PCI attestation — spanning the full range of requirements most financial services firms encounter across product lines.

| Category | Details |

|---|---|

| Compliance Certifications | SOC 2 Type II, GDPR, HIPAA, PCI AOC |

| Key Features | Visual conversation builder, compliance team approval workflows, proactive behavioral messaging |

| Best For | Banks and credit unions where compliance teams need direct, non-technical control over AI conversation design |

How We Chose the Best Conversational AI for Fintech Compliance

The most common evaluation mistake fintech teams make is applying general chatbot metrics to a compliance-sensitive context. Deflection rate and response time are not the right criteria here.

The CFPB has documented a specific failure mode it calls "doom loops" — where customers get trapped in repetitive, unhelpful AI responses without any path to a human agent. This matters because deflection rate (conversations that didn't reach a human) and resolution rate (issues actually resolved) are different metrics. Optimizing for deflection while neglecting resolution is a documented regulatory concern.

Evaluation Criteria Used

Compliance certification depth

- SOC 2 Type II (not Type I — Type II tests over time, Type I tests at a point in time)

- ISO 27001 for information security management

- ISO 42001 for AI-specific governance — an emerging requirement worth tracking

- PCI DSS where the bot touches cardholder data

Hallucination control architecture

- Proprietary RAG vs. generic embeddings vs. reasoning-first

- Whether guardrails are preventive (by design) or reactive (post-generation filters)

Audit trail granularity

- Full conversation and action logging vs. summary-only

- Timestamp and intent classification on every exchange

- Retention configurations that meet NYDFS Part 500 and OCC requirements

Deterministic workflow controls

- Ability to enforce mandatory disclosures at specific conversation points

- Escalation triggers that cannot be bypassed by AI reasoning

Integration depth

- Compatibility with existing helpdesk, core banking, and CRM systems

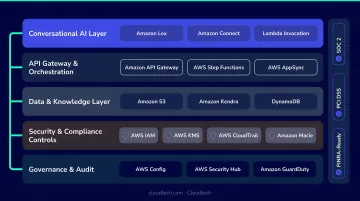

The Infrastructure Layer

Tool selection alone doesn't deliver compliance. Data residency, encryption at rest and in transit, access controls, and audit log retention are all determined by how the AI platform is deployed — not just what certifications the software holds.

AWS-based deployments give fintech teams the configuration controls needed to meet NYDFS Part 500, GDPR data residency requirements, and DORA obligations at the infrastructure layer. AWS CloudTrail provides log file integrity validation using SHA-256 hashing, and AWS Artifact gives teams on-demand access to compliance reports — including SOC 2 and PCI attestations for the underlying infrastructure.

For fintechs deploying conversational AI on AWS, Cloudtech's financial services cloud practice builds out the compliance stack that makes AI governance enforceable at the infrastructure level — not just on paper. That stack typically includes:

- AWS Config for continuous configuration monitoring

- CloudTrail for tamper-evident audit logging

- KMS for encryption at rest and in transit

- IAM for least-privilege access control

Conclusion

There is no single best conversational AI for fintech compliance. The right platform depends on institution size, use case risk profile, existing tech stack, and the regulatory jurisdictions in play. Kasisto leads for banking specialization. Twig stands out on audit trail design. Fini offers the strongest hallucination control architecture. Kore.ai handles enterprise scale. Ada gives compliance teams the most direct non-technical control.

One thing holds across every platform: compliance certifications are a baseline, not a guarantee. A SOC 2 Type II report means the vendor was audited — it doesn't mean the platform handles escalation correctly or produces audit trails your regulators will accept.

Before you sign with any vendor, run these three checks:

- Demand the actual audit report, not the badge on the marketing page

- Test against regulated query scenarios — dispute claims, fraud reports, fee waivers — and document how the system responds

- Evaluate escalation behavior as a compliance control, not just a UX feature

If you've selected your conversational AI platform and need to deploy it on AWS infrastructure that meets the same compliance standards as the tool itself, connect with Cloudtech's AWS consulting team. We help financial services companies build the cloud foundation — encryption, audit logging, access controls, data residency — that makes AI governance actually enforceable.

Frequently Asked Questions

What is the best conversational AI for fintech compliance?

The answer depends on your use case. Kasisto leads for banking-domain specialization, Twig for audit trail depth, Fini for regulated decision traceability, Kore.ai for enterprise multi-channel deployments, and Ada for no-code compliance team control. Across all options, SOC 2 Type II certification and demonstrable audit trails are baseline requirements.

What compliance certifications should a fintech conversational AI platform have?

The minimum stack is SOC 2 Type II, ISO 27001, and GDPR compliance. Add PCI DSS v4.0.1 if the bot touches cardholder data, and HIPAA for health-adjacent financial products. ISO 42001, the emerging AI management system standard, is increasingly referenced by regulators for AI-specific governance.

How do conversational AI tools handle KYC and AML compliance?

Compliant platforms classify KYC and AML queries as high-risk and refuse autonomous resolution. Instead, they escalate with full conversation context, intent classification, and confidence scores to human agents. Every step in that escalation chain must be captured in the audit trail for regulatory review.

What is the difference between deflection rate and resolution rate for fintech AI?

Deflection counts conversations that didn't reach a human, including abandoned ones where nothing was resolved. Resolution rate measures whether the customer's issue was actually solved. The CFPB has flagged deflection-focused chatbot design as a compliance risk when it blocks customers from accessing human support or asserting federal rights.

What regulations govern conversational AI use in financial services?

Key frameworks include CFPB consumer protection rules, OCC Bulletin 2023-17 on third-party risk, NYDFS Part 500 cybersecurity requirements, and GDPR Article 22 for EU customers. The EU AI Act classifies creditworthiness and insurance AI as high-risk, with full obligations applying from August 2, 2026.

How does cloud infrastructure affect conversational AI compliance in fintech?

A platform's compliance certifications only cover the software layer. Data residency, encryption, access controls, and audit log retention are all determined by the underlying cloud deployment. AWS provides the controls needed for NYDFS Part 500, DORA, and GDPR — CloudTrail, KMS, Config, IAM — but they must be correctly configured by whoever deploys the system.