Introduction

Most insurance companies deploying AI chatbots face the same uncomfortable reality: they went live with a clear sense of what they wanted the bot to do, but little structured way to confirm it's actually doing it. The chatbot handles some volume, escalation rates look acceptable on paper, and no one has complained loudly. That silence is routinely mistaken for success — and it rarely is.

Accenture estimates that poor claims experiences could put up to $170 billion in global insurance premiums at risk by 2027. A chatbot that frustrates claimants, misroutes policy queries, or misses required disclosures doesn't just cost you a satisfaction score — it costs you renewals, exposes you to regulatory risk, and erodes trust when customers need you most.

What follows is a practical evaluation framework built for insurance: the metrics that reveal real performance, the compliance checkpoints most vendors skip, and how to build measurement into ongoing operations — not just launch day.

Key Takeaways

- Containment rate is the most misread metric; always filter out unintended escalations before drawing conclusions

- Insurance chatbots require a second layer of evaluation beyond universal metrics: FNOL completion rate, ID&V automation rate, and compliance adherence

- Baseline metrics must be established before or at launch — evaluation without a baseline makes ROI impossible to prove

- Hallucination risk is especially acute in insurance — incorrect coverage information carries real legal and reputational consequences

- Effective oversight combines automated monitoring with periodic manual review; one without the other leaves gaps

What AI Chatbot Evaluation in Insurance Actually Involves

AI chatbot evaluation is the systematic process of measuring how a conversational AI system performs against defined operational, experience, and business objectives. That covers intent recognition accuracy, task completion rates, compliance adherence, and integration reliability — measured across real interactions, not just test scenarios.

Insurance chatbot evaluation differs from general chatbot evaluation in two meaningful ways.

First, the stakes of failure are higher. A retail chatbot that misfires frustrates a customer. In insurance, the same failure can mishandle a first notice of loss submission during a distressing claim event, deliver non-compliant policy language, or expose sensitive personal data through a failed ID&V check.

Second, the success criteria are more complex. General chatbot metrics measure whether a conversation resolved. Insurance metrics go further — they must also capture:

- Whether the bot correctly guided a multi-step FNOL workflow

- Whether identity verification completed without requiring an agent handoff

- Whether every required disclosure was captured

Offline vs. Online Evaluation

Each approach serves a different stage of deployment:

- Offline evaluation uses pre-collected data or simulation — useful during development to catch intent coverage gaps before launch

- Online evaluation measures real interactions in production — the gold standard for insurance, because real claim and policy scenarios surface edge cases that simulation cannot replicate reliably

In production, real claim and policy interactions will always surface gaps that test data misses — which is why online evaluation carries more weight once a system goes live.

Key Performance Metrics for Insurance AI Chatbots

These are the foundational metrics every insurance chatbot evaluation framework needs, regardless of vendor or use case. Without them, you cannot benchmark improvement or prove ROI.

Containment Rate

Containment rate measures the percentage of conversations the chatbot resolves end-to-end without human intervention — the clearest measure of how much the bot can handle on its own.

The critical nuance: not all contained conversations are successes, and not all escalations are failures.

There are two types of escalations:

- Intended escalations — complex underwriting queries or emotionally distressed customers the bot is designed to hand off

- Unintended escalations — bot failures, user frustration, or dead-end conversation flows

Conflating these inflates your containment number and masks real performance gaps. Tag escalations by reason — user-requested, bot-triggered, compliance-mandated — and track unintended escalations as a separate KPI.

Goal Completion Rate

Here's the question containment rate can't answer: did the user actually accomplish what they came to do?

A conversation can be "contained" and still fail completely. The user who starts an FNOL submission, hits a dead end, and closes the chat without filing is counted as contained in many implementations. Goal completion rate catches that failure.

Track this per workflow: quote requests, FNOL submissions, identity verification, claims status checks. Each has a distinct completion definition.

NLU Accuracy and Intent Recognition Rate

NLU accuracy measures how consistently the chatbot correctly identifies what the user is asking. In insurance, users phrase the same request dozens of different ways — "I need to report an accident," "my car got hit," "I want to start a claim" — and the bot must map all of them to the right intent.

In a regulated context, misclassification isn't just a bad user experience. It can:

- Route customers to the wrong workflow entirely

- Trigger a non-compliant response path

- Create audit risk if the bot acts on incorrect intent in a claims or coverage context

Monitor intent recognition rate across all active intents, and flag any intent where fallback or misclassification rates spike above your defined threshold.

Average Handle Time and Response Latency

AHT covers total conversation duration from initiation to resolution. Latency is the delay between user input and bot response.

Insurance interactions frequently involve backend system lookups — policy retrieval, claims status checks, identity verification against CRM records. Each lookup adds latency. Where your bot's infrastructure is hosted relative to your backend systems matters: integrations that cross regions or traverse multiple API layers compound delays. When evaluating vendors, ask specifically how their architecture handles high-concurrency lookup requests and what their p95 response time looks like under load.

There is no single published industry benchmark for acceptable insurance chatbot latency. Establish your own baseline at launch and track against it.

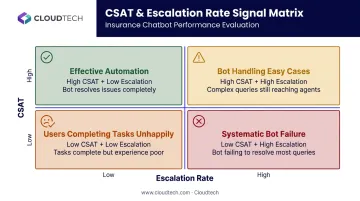

CSAT and Escalation Rate

Track these together — the combination tells a more complete story than either alone:

| Signal | Interpretation |

|---|---|

| High CSAT + low escalation | Effective automation |

| Low CSAT + high escalation | Systematic bot failure |

| High CSAT + high escalation | Bot handling easy cases; complex ones reaching agents |

| Low CSAT + low escalation | Users completing tasks but unhappily |

Industry confidence data offers useful context here: Corporate Insight found that only 12% of auto insurance customers were very or extremely confident in chatbots, with 66% disconnecting after realizing they were talking to a bot. That trust gap makes CSAT tracking especially consequential in insurance deployments.

Insurance-Specific Evaluation Criteria

General metrics tell you how a chatbot is performing — insurance-specific criteria tell you whether it's performing correctly for your industry's requirements. Most generic evaluation frameworks skip this layer entirely.

ID&V Automation Rate

ID&V automation rate measures the percentage of customer identity checks completed fully by the chatbot — no agent required.

Identity verification is nearly universal across insurance interactions. It happens at the start of claims calls, policy inquiries, and payment updates. That makes it both the highest-volume automation opportunity and a high-stakes accuracy requirement.

Cognigy reports that one unnamed Fortune 100 insurer handling 20 million calls annually achieved approximately 95% automation for ID&V, with human involvement in fewer than 5% of cases — saving roughly 90 seconds per call. That's a useful benchmark for what well-implemented ID&V automation looks like at scale.

FNOL Completion Rate

FNOL completion rate tracks the percentage of first notice of loss workflows the chatbot guides users through successfully — without abandonment or agent takeover.

FNOL is one of the harder workflows to automate well. The customer has just experienced an accident, a flood, or a theft — emotional state is high and patience is low. The workflow is multi-step and documentation-heavy, so a bot that fails partway through doesn't just frustrate the user; it delays downstream claim processing.

Measure FNOL completion rate alongside data completeness — did the chatbot collect all required fields? A "completed" FNOL that's missing incident details or documentation creates rework for claims adjusters.

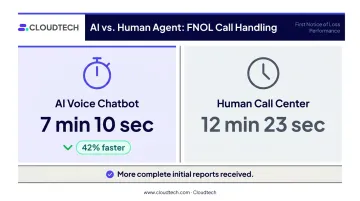

Liberate reports that Branch Insurance's voice AI completed FNOL calls in 7 minutes 10 seconds, compared to 12 minutes 23 seconds for their outsourced human call center — a 42% reduction in handle time. Claims representatives also reported receiving more complete initial reports.

Compliance and Consent Capture Rate

This metric tracks the percentage of interactions where the chatbot:

- Records required user consents

- Delivers mandated policy disclosures

- Follows jurisdiction-specific regulatory scripts

In the US, the NAIC Model Bulletin (adopted 2023) expects insurers using AI systems in consumer-impacting decisions to maintain a written AI Systems Program, governance controls, testing documentation, and consumer notice processes. State-level adoption varies — New York's Circular Letter No. 7 and Colorado's Regulation 10-1-1 establish additional requirements in their respective jurisdictions.

For European insurers, GDPR governs consent validity: it must be freely given, specific, informed, and expressed through affirmative action.

A missed disclosure carries audit risk and potential liability — not just a degraded user experience. Review this metric on every deployment handling FNOL or coverage queries.

Policy Adherence and Hallucination Risk

For AI-powered chatbots using large language models or generative AI, policy adherence rate measures how consistently the bot's responses align with approved product language, legal disclaimers, and factual policy details.

The hallucination risk is real and well-documented in insurance. EIOPA's survey of 347 European insurance undertakings identified hallucinations as the most-cited generative AI risk — ahead of cybersecurity and data protection concerns.

The stakes are higher in insurance than in most industries. A customer who receives an incorrect answer about their coverage or claim eligibility may act on it — and if that error traces back to the chatbot, the insurer carries the exposure.

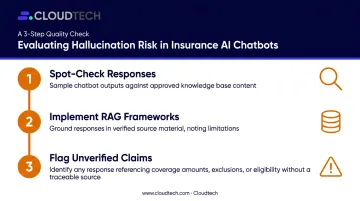

How to evaluate for hallucination risk:

- Spot-check chatbot responses against approved knowledge base content on a sampled basis

- Implement retrieval-augmented generation (RAG) frameworks to ground responses in verified source material — AWS notes that RAG can improve accuracy but does not eliminate hallucinations entirely

- Flag any response that references specific coverage amounts, exclusion terms, or claim eligibility without a traceable source document

How to Run an AI Chatbot Evaluation: Step by Step

Metrics alone aren't enough. Evaluation requires a structured process, and it needs to be built in before launch, not retrofitted after the fact.

Step 1 — Define Scope and Use Cases

Identify which workflows the chatbot handles and what success looks like for each:

- FNOL: Primary metric is completion rate plus data completeness

- ID&V: Primary metric is automation rate and verification accuracy

- Policy queries: Primary metric is NLU accuracy and compliance adherence

- Claims status: Primary metric is goal completion rate and AHT

Different workflows require different primary metrics. Don't apply a single scorecard to all of them.

Step 2 — Establish Baselines Before Launch

Capture pre-deployment or early-deployment metrics for equivalent human-handled interactions: escalation rate, AHT, CSAT, and task completion rates. These become your comparison point.

Without a baseline, you cannot prove the chatbot improved anything, or detect regression if performance slips.

Step 3 — Run Automated Monitoring in Production

Set up dashboards tracking foundational metrics in real time: containment rate, NLU accuracy, fallback rate, latency, and escalation volume. Online evaluation using real interactions is more reliable than synthetic test sets for insurance, since real claim scenarios and emotional context cannot be simulated accurately.

Security First Insurance deployed a chatbot that handled 30% of all inbound calls received after Hurricane Michael, with 75% of users completing interactions without diversion and average call time falling by more than 75%. Surge scenarios like this are exactly where real-time monitoring proves its value: FNOL completion rates need to hold under load, not just under normal conditions.

Step 4 — Supplement With Manual Review

Automated evaluation catches quantitative failures. Manual review catches everything else: tone mismatches, technically correct but contextually wrong responses, partial compliance, and ambiguous escalation reasons.

Review a sampled set of conversations periodically. For high-volume regulated workflows like FNOL and coverage queries, weekly review is appropriate. Human judgment catches what metrics cannot.

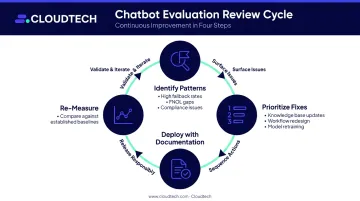

Step 5 — Act, Iterate, and Re-Evaluate

The review cycle:

- Identify patterns: high fallback rates on specific intents, low FNOL completion on mobile, compliance gaps in a state's disclosure script

- Prioritize fixes by impact: knowledge base updates, workflow redesign, or model retraining

- Deploy changes with documentation for audit purposes

- Re-measure against the same baselines and benchmarks

When this cycle runs consistently, gaps surface early. When it doesn't, compliance failures and falling CSAT scores tend to surface first in customer complaints.

Common Evaluation Mistakes Insurers Make

Three mistakes consistently lead insurance teams to misread chatbot performance — and act on metrics that don't reflect reality.

Misreading Containment Rate

Treating all contained conversations as automation successes inflates your metrics. A user who gives up and closes the chat is counted as "contained" in many implementations — that's not a success, it's an undetected failure.

Fix: Tag every escalation by reason. Measure unintended escalation rate as a separate KPI.

Benchmarking Against Inconsistent Scope

When benchmarking a new AI-powered system against a legacy rule-based bot, direct metric comparison is only valid if both systems cover the same set of automatable workflows and collect the same data points. Differences in scope make the comparison meaningless.

Before benchmarking, align on the exact set of workflows each system covers. Any gap in coverage must be explicitly accounted for — otherwise you're comparing apples to oranges.

Relying on a Single Evaluation Method

Manual review alone doesn't scale and introduces evaluator bias. Automated scoring alone misses nuanced failures, especially in generative AI systems where a response can be grammatically correct, plausible-sounding, and factually wrong at the same time.

Build a hybrid cadence: automated scoring runs continuously, while human reviewers sample 50–100 conversations per week, focusing on escalations, low-confidence responses, and flagged edge cases.

How Cloudtech Can Help

Deploying and evaluating an AI chatbot on AWS in a regulated industry requires more than selecting the right service — it requires architecting for compliance, latency, and integration with existing systems from the ground up.

Cloudtech is an AWS Advanced Tier Partner with hands-on experience in financial services and healthcare, two sectors where the regulatory rigor and data sensitivity requirements closely mirror what insurance carriers face. Their team — 70% former AWS employees — works with services like Amazon Bedrock, AWS security and compliance frameworks, and data modernization infrastructure as infrastructure components in production AI architectures.

Cloudtech's engagements start with structured discovery and planning phases that define compliance requirements, security controls, and success criteria before any deployment begins. That pre-deployment structure is what makes evaluation frameworks reliable and auditable from day one — not retrofitted after launch.

Relevant capabilities Cloudtech brings to insurance AI projects include:

- Compliance-first architecture across HIPAA, SOC 2, and financial services requirements

- Generative AI implementation on Amazon Bedrock, including RAG pipelines and LLM integration

- Data governance and quality frameworks built for regulated environments

- AWS security and audit controls aligned with production deployment standards

In healthcare environments — including work for a nonprofit healthcare insurer that reduced root cause analysis time by 80% — Cloudtech has demonstrated the ability to deliver measurable operational outcomes within compliance-driven constraints that directly parallel insurance requirements.

For insurers evaluating chatbot performance or planning a new deployment, that foundation matters: evaluation frameworks built into the architecture from day one produce more reliable, auditable results.

Conclusion

Evaluating an AI chatbot in insurance is an ongoing strategic practice — one that protects customer trust, supports regulatory compliance, and gives leadership a clear picture of what their automation investment is actually delivering.

A complete framework covers both layers: universal performance metrics like containment rate and CSAT, plus insurance-specific measures such as FNOL completion rate, ID&V automation rate, and compliance adherence. Skipping either layer leaves real gaps.

Teams that outperform consistently share a specific habit: they define success criteria before launch, establish measurable baselines, and schedule regular review cycles rather than treating evaluation as a post-deployment afterthought.

Frequently Asked Questions

What are the most important metrics for evaluating an AI chatbot in insurance?

The foundational metrics are containment rate, NLU accuracy, goal completion rate, and CSAT. Layer on top of these the insurance-specific criteria: FNOL completion rate, ID&V automation rate, and compliance consent capture rate. Both layers are required for a complete picture.

How is containment rate different from goal completion rate for insurance chatbots?

Containment rate measures whether the bot handled the conversation without human intervention. Goal completion rate measures whether the user actually achieved their intended outcome — such as filing a claim or verifying their identity. A conversation can be fully contained and still fail to meet the user's goal.

What compliance metrics should insurers track when evaluating AI chatbot performance?

Track consent capture rate, policy adherence rate, and disclosure accuracy. These metrics protect insurers from audit risk under frameworks like the NAIC Model Bulletin and state-level AI guidance, and are especially critical for deployments handling FNOL or coverage queries.

How often should insurance companies review AI chatbot performance metrics?

Run automated monitoring daily for operational KPIs like escalation rate and fallback rate. Review intent accuracy trends weekly. Monthly, run evaluation cycles with manual sampling of conversation transcripts — especially for regulated workflows.

What are the most common mistakes insurers make when evaluating AI chatbot performance?

The two most damaging: misinterpreting containment rate by counting user abandonment as successful automation, and benchmarking chatbot implementations that have different workflow scope or business logic — making the comparison invalid before it starts.

How do I know if my insurance AI chatbot is ready to scale?

Four signals indicate readiness: sustained high NLU accuracy across production traffic, stable or declining unintended escalation rates, consistent FNOL and ID&V completion rates under load, and no compliance gaps surfaced during manual review. If any one signal is weak, the deployment isn't ready to scale.