That pressure is intensifying. Insurtech funding rebounded to $5.08 billion in 2025, up nearly 20% year-over-year, signaling renewed competitive intensity from technology-first challengers. Meanwhile, Accenture's survey of 49,000 insurance consumers found that 60% would share personal data in exchange for faster claims processing — but 76% remain worried about how that data gets used.

Generative AI sits at the center of how insurers are responding. This guide covers what Gen AI actually does in an insurance context, where it delivers the most value across the insurance value chain, what risks require governance before scaling, and how to build the cloud foundation that makes deployment possible.

Key Takeaways

- Gen AI handles insurance's most stubborn inefficiencies: document-heavy underwriting, complex claims workflows, and high-volume customer service

- The highest-impact use cases span underwriting, claims management, policy administration, and sales

- McKinsey projects Gen AI could unlock $50–$70B in insurance revenue — marketing and sales lead the way

- Hallucinations, regulatory scrutiny, and data fragmentation are the three risks that derail most deployments

- Cloud infrastructure — particularly AWS — must be in place before Gen AI can scale reliably

What Is Generative AI in Insurance?

Generative AI in insurance refers to AI systems — typically large language models (LLMs) — that interpret and produce natural language, summaries, and structured outputs from complex inputs like policy documents, claims files, underwriting notes, and call transcripts.

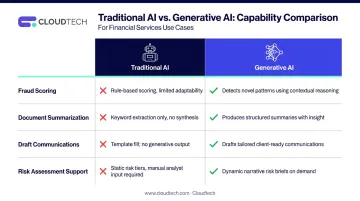

How It Differs from Traditional AI

Traditional AI classifies or scores within predefined rules. A fraud detection model flags claims that hit certain criteria; it doesn't read context, draft responses, or interpret context across multiple documents. Generative AI reads unstructured content and generates outputs: a summary of a 40-page commercial property submission, a draft settlement letter, an answer to a policyholder's coverage question in plain English.

| Capability | Traditional AI | Generative AI |

|---|---|---|

| Fraud scoring | ✅ Classifies within rules | ✅ Also flags narrative inconsistencies |

| Document summarization | ❌ Requires structured input | ✅ Handles unstructured text natively |

| Draft communications | ❌ Template-only | ✅ Generates contextual responses |

| Risk assessment support | ✅ Scores known variables | ✅ Synthesizes novel risk profiles |

Three Gen AI Approaches Relevant to Insurance

- LLMs for document summarization, knowledge search, and customer-facing chatbots

- Multimodal models that analyze images alongside text — useful for property damage assessment combining photos with claim narratives

- Retrieval-Augmented Generation (RAG), which grounds AI outputs in the insurer's own policy documents, underwriting guidelines, and knowledge bases — reducing hallucination risk and ensuring answers reflect actual policy terms rather than model assumptions

In regulated insurance contexts, RAG's emphasis on accuracy and auditability makes it the most practical starting point for most deployments.

Key Generative AI Use Cases Across the Insurance Value Chain

Gen AI touches every stage of the insurance value chain — from policy sales and underwriting through administration and claims. The technology doesn't just optimize individual tasks; it redesigns entire workflows end to end.

Underwriting

Underwriters spend significant time doing work that isn't underwriting. Accenture's survey of P&C underwriters found that 40% of work time went to administrative tasks — leaving only 30% for actual risk evaluation. Gen AI targets that imbalance directly.

By ingesting structured and unstructured inputs — loss data, applicant records, external risk signals — Gen AI produces concise risk summaries that let underwriters focus on judgment rather than document excavation. AWS reports that EXL's Gen AI underwriting assistant, built on Amazon Bedrock, helped insurance clients reduce underwriting costs by 80%.

A practical example: cyber insurance underwriting. Gen AI can analyze a company's digital footprint, security posture, and breach history, then generate a customized risk profile and draft tailored policy recommendations in a fraction of the time a manual review requires.

Swiss Re's Life Guide Scout, launched in April 2024, demonstrates this in production. The Gen AI assistant answers natural-language underwriting questions in seconds, pulling from curated knowledge bases and citing the source for each answer.

Claims Management

Claims is where Gen AI's document-processing capabilities translate most directly into dollars. Bain projects that fully applied Gen AI could reduce P&C loss-adjusting expenses by 20–25%, creating more than $100 billion in value industry-wide.

The applications span the full claims lifecycle:

- FNOL intake — Automatically extracting and routing information from first notice of loss documents, emails, and forms

- Document analysis — Allianz's Insurance Copilot gathers claims and contract data, summarizes files, analyzes images, compares claims against policy terms, and flags discrepancies across invoices and incident descriptions

- Settlement drafting — Generating communications to policyholders based on claim outcomes

- Fraud detection — Surfacing inconsistencies across claim narratives, images, and historical patterns for human review

Allianz's agentic AI for food-spoilage claims reduced processing from days to hours — compressing cycle time in ways that cut costs and improve customer satisfaction at the same time.

Sales, Distribution & Customer Service

Gen AI enables two distinct capabilities on the revenue side:

- Personalized marketing — Analyzing customer segments to generate tailored campaign content, policy recommendations, and retention outreach. Deloitte documents this as a primary insurance Gen AI use case, alongside hyper-personalized product recommendations.

- 24/7 customer service — A survey reported by Insurance Journal found that 63% of UK insurers had already deployed Gen AI chatbots in customer service operations. These systems handle complex policy questions in natural language, reducing call center volume while extending service availability beyond business hours.

Policy Administration & Risk Management

Policy administration is document-heavy by nature — issuance, renewals, endorsements, compliance communications. Gen AI automates drafting and processing across these workflows, reducing administrative overhead and the human error that compliance teams spend time correcting.

Cleaner administration also feeds better risk modeling. Gen AI supports scenario simulation and synthetic data generation — McKinsey identifies synthetic-data risk modeling in life insurance and simulated loss scenarios in commercial P&C as active use cases, particularly useful when historical data on rare or emerging risk categories is thin.

Business Benefits of Generative AI for Insurers

McKinsey estimates Gen AI could unlock $50–$70 billion in insurance industry revenue, with the largest opportunity in marketing and sales. But the value case isn't just top-line.

Three dimensions matter:

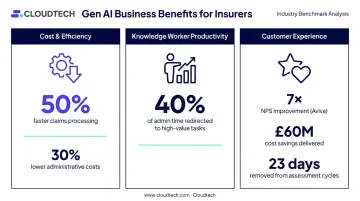

Cost and efficiency — Automating document-heavy tasks reduces processing costs. Cloudtech's IDP engagements have documented 50% faster claims processing and up to 30% lower administrative costs for insurance clients, driven by automated extraction from policy and claims documents.

Knowledge worker productivity — Underwriters, claims adjusters, and customer service agents all spend disproportionate time on information retrieval and documentation. Gen AI redirects that effort toward higher-value judgment calls. A team that spent 40% of its time on admin tasks can redirect that capacity toward risk evaluation and relationship management.

Customer experience — Faster claims resolution, multilingual 24/7 support, and personalized policy guidance translate into measurable NPS and retention improvements. Aviva's AI claims program, deploying more than 80 models across motor claims, achieved a sevenfold NPS improvement, removed 23 days from complex liability assessments, and saved more than £60 million (roughly $76 million) in 2024.

Deloitte's June 2024 survey of 200 US insurance executives found 76% had implemented Gen AI in at least one function. Only 45% believed benefits currently outweighed risks, meaning governance and infrastructure readiness — not model capability — remain the primary constraint.

Challenges and Risks Insurers Must Navigate

The Hallucination Problem

Gen AI models can generate plausible but incorrect outputs. In a customer-facing insurance context — where a misstatement about coverage terms creates real liability — this isn't a theoretical concern. It's a governance requirement.

RAG architectures reduce this risk by grounding outputs in verified documents rather than open model generation. Human-in-the-loop review is the other essential safeguard, particularly for any output that informs a coverage or payment decision.

Regulatory Scrutiny

The US regulatory environment is active and accelerating:

- The NAIC Model Bulletin on AI Systems (adopted December 2023) sets expectations for written AI governance programs, risk controls, testing, and documentation. 19 states had adopted it by early 2025.

- New York DFS Circular Letter No. 7 (July 2024) requires governance, testing for unfair discrimination, explainability, and consumer notice for AI used in underwriting and pricing.

- Colorado SB 21-169 authorizes rules against unfair discrimination from algorithms and predictive models.

- California Bulletin 2022-5 states that AI bias in marketing, rating, underwriting, and claims will be investigated under existing insurance law.

No single federal AI insurance law exists yet, but state-level momentum is significant. Insurers must maintain audit trails and demonstrate decision transparency — not just for regulators, but for the policyholders who will increasingly ask how AI influenced their outcomes.

Data and Infrastructure Readiness

Many insurers run on legacy systems where data is fragmented across policy administration, claims, billing, and CRM platforms. Unified, cloud-integrated data pipelines are a prerequisite for Gen AI deployment — and this foundational work is consistently underestimated.

Deloitte identified data readiness as the weakest point in most insurers' Gen AI preparedness. Building the infrastructure to connect and govern data across systems isn't glamorous, but it determines whether models ever deliver value in production.

How to Get Started: Building a Gen AI-Ready Foundation

Start with Internal, Low-Risk Use Cases

The safest first deployments are internal and information-intensive:

- Underwriter document summarization — Compress submission documents into structured risk summaries for human review

- Internal knowledge search — Let underwriting and claims teams query policy guidelines and procedure documents in natural language

- Claims document extraction — Automate the pull of key data points from FNOL documents and medical records

These "horizontal" use cases build organizational confidence, surface data quality issues, and generate the institutional knowledge needed before tackling customer-facing applications.

Establish Governance Before Scaling

A governance framework isn't something to retrofit after a pilot succeeds. Define it early:

- Assign clear accountability for AI output quality

- Set up monitoring for accuracy drift and bias

- Document data lineage so every AI-assisted decision is traceable

- Align with NAIC and applicable state guidance on explainability requirements

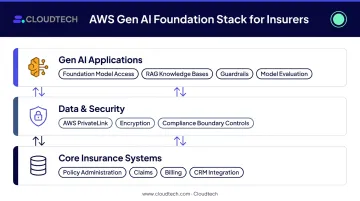

Build on the Right Cloud Foundation

Gen AI requires scalable compute, secure data pipelines, and integration with existing core systems. AWS offers the infrastructure layer that makes this possible:

- Amazon Bedrock provides managed access to multiple foundation models, RAG via Knowledge Bases, Guardrails for content filtering, and model evaluation — without requiring model infrastructure management

- AWS data protection controls ensure prompts and completions are not shared with model providers or used to train base models

- AWS PrivateLink and encryption keep data within the insurer's compliance boundary

Insurers without a modern cloud foundation should treat that as the first milestone, not a parallel workstream.

Cloudtech, an AWS Advanced Tier Partner staffed primarily by former AWS engineers, helps insurance organizations build that foundation. The team delivers data readiness assessments and pre-packaged AWS solutions in as little as two to eight weeks, giving SMBs a clear path from initial assessment to production GenAI without the cost structure of a large enterprise engagement. If your organization is ready to assess where you stand and what comes next, connect with the Cloudtech team for a direct conversation.

Frequently Asked Questions

How is Gen AI used in insurance?

Gen AI is applied across underwriting support, claims processing, AI-driven customer service, personalized marketing, policy administration, and risk scenario modeling. All these use cases center on handling unstructured documents and producing outputs — summaries, recommendations, communications — that previously required manual effort.

What is the difference between traditional AI and generative AI in insurance?

Traditional AI classifies or scores within defined rules — for example, a fraud scoring model flagging suspicious claim patterns. Gen AI generates new content and synthesizes context across open-ended tasks, such as summarizing medical records, drafting settlement letters, or answering policyholders' natural-language coverage questions.

What are the biggest risks of using generative AI in insurance?

The primary risks are hallucinations (plausible but incorrect outputs in regulated contexts), data privacy and cybersecurity exposure from deploying models on sensitive claims data, and bias propagation from historically skewed training data. Each requires active governance and human oversight.

Which insurance processes benefit most from generative AI?

Claims management and underwriting offer the highest immediate impact due to their document intensity and the cost of manual processing. Customer service and policy administration follow closely, with Gen AI enabling 24/7 support and automating high-volume administrative workflows.

Is generative AI regulated in the insurance industry?

No single federal AI insurance law exists in the US, but regulation is advancing quickly. The NAIC Model Bulletin — adopted by 19 states — requires written AI governance programs, testing, and documentation. Several states, including New York and California, have added further guidance on explainability and non-discrimination.

How long does it take to implement generative AI in an insurance company?

Timelines depend heavily on cloud and data readiness. Internal pilot use cases — document summarization, knowledge search — can often be deployed in weeks with the right infrastructure in place. Enterprise-scale rollouts typically take several months, driven by governance framework development and legacy system integration.