Introduction

Traditional credit risk models were built for a world where structured financial data — credit scores, debt ratios, income statements — told most of the story. That world no longer exists.

Today's borrowers leave digital footprints across financial statements, court filings, news articles, email threads, and e-commerce histories. Legacy scoring systems cannot read these sources. The result: blind spots that cost lenders money and exclude borrowers who are genuinely creditworthy.

Manual credit review compounds the problem. Multi-day review cycles, inconsistent analyst judgments, and periodic portfolio snapshots mean risk often surfaces only after it becomes a loss.

A 2024 McKinsey survey of 24 financial institutions found that 20% had already implemented at least one generative AI use case in credit risk, with 60% expecting to do so within a year. Lenders that delay are ceding ground to those that don't.

This guide covers what generative AI actually means in the credit context, the highest-impact use cases across the credit lifecycle, measurable benefits, real challenges, and a practical five-step implementation framework for financial services teams.

Key Takeaways

- Gen AI draws insights from unstructured data (documents, news, communications), not just structured financial records

- Highest-ROI use cases include automated credit analysis, alternative data processing, fraud detection, and real-time portfolio monitoring

- Credit decisioning time drops dramatically with Gen AI — often by 70–80% — while improving accuracy and reaching underserved borrowers

- Successful deployment depends on data readiness, cloud infrastructure, explainability frameworks, and a scoped pilot before full rollout

- Regulatory compliance must be designed into Gen AI systems from day one — not retrofitted after deployment

What Is Generative AI in Credit Risk Management?

Generative AI in this context means using large language models (LLMs) and foundation models to synthesize, reason across, and generate insights from both structured and unstructured data. Unlike traditional ML — which classifies risk using labeled historical records — generative AI can read a 200-page annual report, extract key risk factors, and produce a structured credit summary in seconds.

The "generative" label matters here: these models produce new outputs — summaries, assessments, recommendations — rather than simply returning a score.

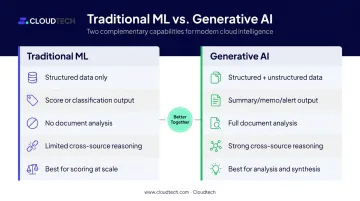

How It Differs from Traditional Credit AI

| Capability | Traditional ML | Generative AI |

|---|---|---|

| Primary data type | Structured (income, FICO, DTI) | Structured + unstructured |

| Primary output | Score or classification | Summary, memo, alert |

| Document analysis | No | Yes |

| Cross-source reasoning | Limited | Strong |

| Best for | Scoring at scale | Analysis, synthesis, monitoring |

The two approaches work together. Traditional ML handles high-volume predictive scoring; Gen AI takes over the qualitative synthesis that previously required hours of analyst time. Understanding where each fits is the starting point for deploying them effectively.

Where Gen AI Fits Across the Credit Lifecycle

- Origination: Application analysis, document processing, fraud screening

- Underwriting: Risk assessment, scoring augmentation, credit memo generation

- Monitoring: Portfolio surveillance, early warning signal detection

- Collections: Borrower communication, recovery prioritization

Key Use Cases of Generative AI in Credit Risk Management

Automated Credit Analysis and Document Intelligence

Gen AI models can ingest financial statements, tax filings, earnings call transcripts, and analyst reports — then produce structured credit memos in a fraction of the time it takes a human analyst. This shifts the analyst's role from data gatherer to decision reviewer, dramatically increasing throughput without sacrificing rigor.

One documented example: a bank's Gen AI credit tool reduced the time needed to answer commercial climate-risk questions by approximately 90%, dropping from over two hours to under 15 minutes, with 90% accuracy on answers.

LLMs also cross-reference multiple documents simultaneously to flag inconsistencies — for example, revenue figures that differ between a loan application and a bank statement. Done manually, this step is slow and error-prone.

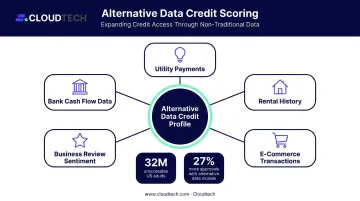

Alternative Data Processing for Broader Credit Access

Approximately 32 million US adults are either credit invisible or hold thin/unscoreable credit files, according to Federal Reserve research. That's a population that traditional scoring models largely cannot serve.

Gen AI can process non-traditional data sources to build richer borrower profiles:

- Utility payment records

- Rental history

- E-commerce transaction patterns

- Business review sentiment

- Cash flow data from bank accounts

The financial inclusion case is also a commercial one. A CFPB-published pilot showed Upstart's alternative data model approved 27% more applicants with 16% lower average APRs than its traditional model — demonstrating that serving thin-file borrowers can be both inclusive and profitable.

Fraud Detection and Anomaly Identification

US lenders had more than $3.3 billion in exposure tied to synthetic identities at the end of 2024. SMB lending fraud grew 13.6% year over year in 2023, with only 27% of fraudsters detected at origination.

Gen AI detects synthetic identity fraud by identifying subtle inconsistencies across unstructured inputs:

- Mismatched address histories across documents

- Income-to-lifestyle ratios that don't add up

- Fabricated or inconsistent supporting documents

- Behavioral signals that contradict stated financial profiles

Rules-based filters catch known patterns — but novel fraud strategies consistently slip through. Gen AI closes that gap by reasoning across context, not just matching against a fixed ruleset.

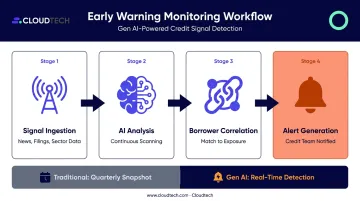

Real-Time Portfolio Monitoring and Early Warning Systems

Portfolio monitoring was the leading Gen AI activity in McKinsey's survey, pursued by nearly 60% of surveyed institutions. Traditional periodic reviews identify deterioration after it becomes a loss. Gen AI catches it earlier.

Continuous scanning of external signals enables proactive risk management:

- News feeds and press releases about borrower companies

- Court filings and regulatory actions

- Supplier and customer relationship changes

- Sector-level macroeconomic shifts

When correlated with individual borrower exposure, these signals generate alerts that give credit teams time to act — not just react.

Regulatory Document Summarization and Compliance Support

Compliance teams can use Gen AI to parse dense regulatory texts — Basel III updates, CFPB guidance, state lending laws — then automatically extract obligations, flag changes, and map them to internal policies. This cuts the manual burden of regulatory horizon scanning considerably.

That burden is only growing. Three active AI law timelines currently affect credit decision systems in the US:

- Colorado: AI law effective January 1, 2027

- California: ADMT compliance requirements beginning January 1, 2027

- New York: Pending legislation under active consideration

Benefits of Generative AI in Credit Risk Management

Gen AI delivers four compounding advantages in credit risk: faster decisions, broader credit access, lower operating costs, and earlier risk detection. Each reshapes a different layer of how credit teams operate.

Faster, More Consistent Decisions

IACPM and McKinsey research covering 44 financial institutions found Gen AI-assisted credit memo drafting produced 20%–60% analyst productivity gains and approximately 30% faster decisioning in documented case examples. These are case-level outcomes, not averages — but they show what's achievable.

Consistency matters as much as speed. Gen AI applies credit policy uniformly across every application, eliminating the analyst variability that creates fair lending exposure.

Expanded Access to Creditworthy Borrowers

Evaluating alternative data through Gen AI extends credit access to individuals and businesses that structured-data models exclude. With roughly 32 million unscoreable adults in the US, even modest improvements in thin-file approval rates represent a significant commercial opportunity — not just a social benefit.

Scalable Cost Efficiency

Automating credit memo generation, document review, and portfolio surveillance reduces analyst labor and lets credit teams manage larger portfolios without proportional headcount growth. That productivity gain translates directly into capacity: more applications reviewed, more accounts monitored, same team size.

Proactive Risk Management

The shift from reactive to proactive is the clearest structural benefit. Early warning systems that surface deterioration signals weeks before default reduce charge-offs and improve portfolio quality. Traditional quarterly reviews — static snapshots taken after the fact — can't match that response window.

Challenges and Risks to Consider

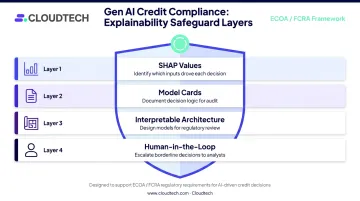

Explainability and the "Black Box" Problem

Under ECOA and the Fair Credit Reporting Act, creditors must provide specific reasons for adverse credit actions. Gen AI models are inherently difficult to interpret. Regulators don't adjust that standard based on model complexity.

Solving this requires deliberate architecture choices upfront:

- SHAP values to identify which inputs drove a decision

- Model cards documenting decision logic

- Regulation-ready model architectures designed for interpretability

- Human-in-the-loop review for borderline decisions

Note: the CFPB's 2022 and 2023 circulars on AI adverse action notices were withdrawn in May 2025, but the underlying ECOA and Regulation B obligations remain fully in force.

Bias and Fairness Risks

Gen AI models trained on historical credit data can inherit and amplify existing biases — systematically underscoring applicants from certain geographies or demographics. This is a documented risk in any model built on historically biased lending decisions.

Required safeguards:

- Rigorous training data audits before model deployment

- Fairness testing across protected demographic groups

- Ongoing disparity rate monitoring post-deployment

- Regular bias audits as data and model behavior evolve

Regulatory and Operational Risk

The regulatory landscape is evolving on multiple fronts. Federal Reserve model risk guidance (SR 26-2, effective April 2026) explicitly excludes GenAI from its scope for now, treating it as novel and rapidly evolving. State-level AI laws are advancing on different timelines.

Institutions need governance frameworks flexible enough to adapt as rules evolve — and model risk documentation is mandatory for regulated entities regardless of current framework gaps.

How to Implement Generative AI for Credit Risk Management

Step 1: Audit Your Data Landscape

Gen AI effectiveness depends on data readiness first. Inventory both structured data (core banking systems, bureau data, loan origination records) and unstructured data (loan files, financial statements, emails, PDF documents). Identify what inputs exist, where they're stored, and whether they're clean enough for model training or fine-tuning.

Common gaps in SMB financial services environments include inconsistent document formats, siloed data across multiple systems, and unstructured data stored without metadata — all solvable, but you need to map them before making architecture decisions.

Step 2: Select the Right Foundation Model and Cloud Infrastructure

Most financial institutions won't build LLMs from scratch. The practical path is fine-tuning or prompt engineering existing foundation models using proprietary data.

AWS provides the infrastructure most financial services teams need:

- Amazon Bedrock — managed access to foundation models (Anthropic Claude, Amazon Titan, Meta Llama) with security controls that keep data within your VPC

- Amazon SageMaker — model training, evaluation, and deployment

- Amazon S3 + AWS Glue — data storage and ETL pipelines for preparing credit documents for AI ingestion

- Amazon Textract — intelligent document processing for extracting structured information from PDFs and forms

- Amazon Q Business — natural language interface layer for business users

For SMBs and mid-market financial firms without deep in-house cloud expertise, partnering with an AWS consulting firm can compress this setup from months to weeks. Cloudtech, for instance, works with financial services teams on exactly this stack — handling architecture decisions, security configurations, and system integrations under a structured Engage → Discover → Align → Deliver methodology. Their fixed-fee 4–8 week pilot POC delivers a working prototype before any commitment to production scale.

Step 3: Start with a Focused Pilot

Don't attempt full lifecycle transformation in round one. Pick a single, high-value, lower-risk use case:

- Automating credit memo generation from financial statements

- Augmenting fraud flag review with anomaly detection

- Building a document Q&A tool for underwriters

A contained pilot delivers measurable ROI quickly and builds organizational confidence for broader rollout. It also exposes data quality issues and integration challenges in a low-stakes environment.

Step 4: Build Governance and Explainability Into the System

Governance cannot be retrofitted. A minimum viable framework includes:

- Documentation of model inputs, decision logic, and version history

- Audit logging via AWS CloudTrail and AWS Audit Manager for full traceability

- Fairness audits run regularly against protected demographic attributes

- Human-in-the-loop escalation for borderline credit decisions

- Bedrock Guardrails configured at the inference layer to enforce responsible AI controls

Financial services firms also need compliance-aware infrastructure from day one — FINRA, GDPR, and emerging state AI law requirements should be mapped during the architecture phase, not addressed after deployment.

Step 5: Integrate, Monitor, and Scale

Gen AI credit tools must connect to existing systems via APIs — core banking platforms, CRMs, credit decisioning engines. Integration complexity is often underestimated; plan for it explicitly.

Ongoing performance monitoring keeps models accurate and regulators satisfied. Track:

- Precision and recall on fraud detection and early warning alerts

- Disparity rates across demographic groups

- Model drift indicators as data distributions shift over time

- Inference latency to catch performance degradation

AWS services like Amazon CloudWatch and AWS X-Ray provide observability for production Gen AI workloads. Catching model drift early keeps it a routine governance task — left undetected, it escalates into a compliance exposure or a real credit loss.

Frequently Asked Questions

How can generative AI be used in credit risk management?

Gen AI can automate credit memo generation, process unstructured alternative data to evaluate thin-file borrowers, detect synthetic identity fraud, monitor portfolios for early warning signals in real time, and summarize regulatory requirements. It applies across both origination and ongoing portfolio management stages.

Should we embrace generative AI in credit risk management?

The business case is strong: speed, accuracy, cost efficiency, and competitive pressure all point toward adoption. Success depends on having data readiness, governance frameworks, and the right implementation approach in place first. Organizations that skip this foundation consistently struggle to move Gen AI models from pilot into production.

What are the 5 C's of credit risk management?

Character, Capacity, Capital, Collateral, and Conditions. Gen AI strengthens each dimension by enabling richer data analysis — assessing character through behavioral signals, capacity through cash flow data, and conditions through real-time macroeconomic monitoring at a depth structured-data models alone cannot match.

What is the difference between traditional AI/ML and generative AI in credit risk?

Traditional ML classifies risk from structured historical data and produces scores. Gen AI synthesizes and reasons across unstructured sources — documents, news, filings — and generates outputs like summaries and recommendations. They work best as complementary capabilities, not substitutes.

What are the biggest risks of using generative AI for credit risk?

The leading risks are model explainability gaps that create regulatory exposure under ECOA and FCRA, bias inherited from historical training data that can produce unfair outcomes, and an evolving regulatory environment — state AI laws and model risk guidance — that requires active governance to track.

How does cloud infrastructure support generative AI in credit risk?

Cloud platforms provide the scalable compute, secure storage, and managed AI services needed to build and deploy Gen AI credit risk models. AWS services like Amazon Bedrock and SageMaker remove the need for costly on-premise infrastructure while keeping model data within your security boundary, which matters considerably for regulated financial institutions.